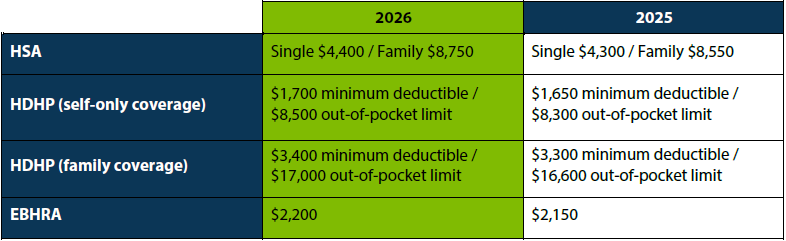

The IRS recently announced the 2026 limits for Health Savings Accounts (HSAs) and High Deductible Health Plans (HDHPs). HSA contribution and plan limits will increase to $4,400 for individual coverage and $8,750 for family coverage. Changes to these limits will take effect January 2026.

HSAs are tax-exempt accounts that help people save money for eligible medical expenses. To qualify for an HSA, the policyholder must be enrolled in an HSA-qualified high-deductible health plan, must not be covered by other non-HDHP health insurance or Medicare, and cannot be claimed as a dependent on a tax return.

Navigating the complexities of the Family and Medical Leave Act (FMLA) can be challenging, especially when it comes to maintaining health coverage for employees on unpaid leave. This guide will help you understand what to do when an employee on FMLA leave fails to pay their health insurance premiums on time, and how it affects Flexible Spending Accounts (FSAs), Health Reimbursement Arrangements (HRAs), Health Savings Accounts (HSAs), and COBRA.

Employer Obligations

Under FMLA, employers must maintain health coverage for employees on leave as if they were still working. This obligation ends if the premium payment is over 30 days late, unless your company policy allows a longer grace period.

Steps Before Dropping Coverage

Before dropping an employee’s health coverage, provide written notice at least 15 days before coverage ends, specifying the termination date if payment isn’t received. Send the notice at least 15 days before the end of the grace period.

Termination of Coverage

Coverage can be terminated retroactively if your company policy allows, otherwise, it ends prospectively at the grace period’s end.

Impact on FSAs, HRAs, and HSAs

FSAs: Employees can choose to continue or revoke their FSA coverage during unpaid FMLA leave. Payment options include pre-pay, pay-as-you-go, and catch-up contributions.

HRAs: Employers must extend COBRA rights to HRAs. Employees can use their HRA balance during COBRA coverage, and employers should calculate a reasonable premium for the HRA.

HSAs: Employees can continue contributing to their HSA during COBRA coverage and use HSA funds to pay for COBRA premiums.

COBRA and ACA Rules

A COBRA election notice isn’t required for coverage loss due to nonpayment. However, failure to return to work after FMLA leave is a COBRA qualifying event. ACA allows cancellation for nonpayment, but stricter state laws may apply.

Restoring Coverage

If an employee returns from FMLA leave after coverage was dropped, their health coverage must be restored.

Managing health coverage for employees on FMLA leave requires careful attention to legal requirements and company policies. By following these steps, you can ensure compliance and support your employees during their leave.

HIPAA special enrollment rights allow eligible employees to enroll in health plans outside the regular enrollment period due to specific life events. These rights also impact Health Reimbursement Arrangements (HRAs), Health Savings Accounts (HSAs), and Flexible Spending Accounts (FSAs).

When and Who Receives the Notice?

Notices must be provided to all eligible employees at or before the time they are first offered the opportunity to enroll. This includes employees who:

Decline coverage due to other health insurance and later lose eligibility.

Become eligible for state premium assistance under Medicaid or CHIP.

Acquire a new spouse or dependent by marriage, birth, adoption, or placement for adoption.

What Should the Notice Include?

The notice must describe special midyear enrollment opportunities and inform participants about deadlines for enrollment requests—30 days for most events, 60 days for Medicaid or CHIP-related events.

Distribution Methods

Include the notice with plan enrollment materials and, if conditions are met, distribute it electronically.

Impact on HRAs, HSAs, and FSAs

Special enrollment rights can affect contributions and usage of HRAs, HSAs, and FSAs:

HRAs: Adjust contributions or usage to align with new coverage.

HSAs: Review HSA contributions and ensure compliance with IRS rules.

FSAs: Update FSA elections to reflect changes in coverage or dependent status.

Consequences of Non-Compliance

Failing to provide the notice timely can lead to enrollment issues and potential penalties from the Department of Labor (DOL).

Providing HIPAA special enrollment notices is essential for compliance and helps employees make informed decisions about their health coverage and financial accounts. Understanding the impact on HRAs, HSAs, and FSAs ensures that employees can effectively manage their health-related financial accounts in conjunction with their health plan enrollment.

Health Savings Accounts (HSAs) are a valuable tool for managing healthcare expenses, especially for those enrolled in high-deductible health plans (HDHPs). However, understanding the contribution limits can be tricky, particularly for married couples with self-only HDHP coverage. In this post, we’ll clarify whether spouses with self-only HDHP coverage can share their HSA contribution limits and provide insights into maximizing their contributions.

HSA Contribution Limits

For 2025, the HSA contribution limits are as follows:

Self-Only HDHP Coverage: $4,300

Family HDHP Coverage: $8,550

Additionally, individuals aged 55 or older can make a “catch-up” contribution of up to $1,000 to their HSA.

Special Rule for Married Individuals

When at least one spouse has family HDHP coverage, a special rule allows the spouses to share the higher family contribution limit. Either spouse’s HSA can receive contributions up to the family maximum, but their combined contributions cannot exceed the family limit. It’s important to note that HSAs are individual accounts, and married couples cannot maintain a joint HSA.

Scenario: Both Spouses Have Self-Only Coverage

In the situation where both spouses have self-only HDHP coverage, the special rule for married individuals does not apply. Each spouse’s contributions will be subject to the self-only limit, including any catch-up contributions if they meet the age requirement. One spouse cannot increase the other spouse’s maximum HSA contributions by contributing less.

Maximizing Contributions

If both spouses with self-only coverage each maintain HSAs and contribute the maximum amount, their aggregate contributions will be slightly more than the family limit ($8,600 versus $8,550). However, they lose the flexibility to place a disproportionate amount of the contribution into one spouse’s HSA. To maximize their aggregate contribution, married couples should:

Maintain two HSAs.

Maximize contributions to each HSA.

Considerations for Choosing Coverage

When deciding whether to elect self-only HDHP coverage from their respective employers or family HDHP coverage from one employer, married couples should consider various factors, including:

Premium costs

Provider networks

Deductible and other cost-sharing amounts

Any spousal surcharges

Understanding HSA contribution limits and rules is crucial for married couples with self-only HDHP coverage. By maintaining individual HSAs and maximizing contributions, they can effectively manage their healthcare expenses. Always consider the broader implications of your HDHP coverage choices to ensure you make the best decision for your financial and healthcare needs.

In today’s competitive job market, offering attractive employee benefits is crucial for retaining top talent. One effective way to enhance your benefits package is by implementing matching Health Savings Account (HSA) contributions through your company’s cafeteria plan. This blog post will guide you through the process, ensuring compliance with relevant regulations and maximizing the benefits for your employees.

Understanding HSA Contributions and Cafeteria Plans

Health Savings Accounts (HSAs) are tax-advantaged accounts that allow employees to save for medical expenses. Contributions to HSAs can be made by both employees and employers. A cafeteria plan, also known as a Section 125 plan, allows employees to make pre-tax salary reduction contributions to various benefits, including HSAs.

Can Employers Make Matching HSA Contributions?

Yes, employers can make matching contributions to employees’ HSAs through a cafeteria plan. However, it’s essential to understand the regulatory requirements to avoid potential pitfalls.

Comparability Requirements vs. Nondiscrimination Rules

Employers’ HSA contributions are generally subject to comparability requirements, which mandate that contributions must be the same dollar amount or the same percentage of the high-deductible health plan (HDHP) deductible for all eligible employees. This standard effectively prohibits matching contributions, as they would trigger a 35% excise tax on the employer.

However, these comparability requirements do not apply to employer HSA contributions made through a cafeteria plan. Instead, such contributions are subject to the Code § 125 nondiscrimination requirements, which include the eligibility, contributions and benefits, and key employee concentration tests. These tests provide more flexibility for employers to vary HSA contributions on a nondiscriminatory basis.

Designing a Compliant Matching Contribution Plan

To ensure compliance with nondiscrimination rules, carefully design your matching contribution plan. Consider the following:

Eligibility: Ensure that all eligible employees have the opportunity to participate in the HSA matching program.

Contribution Limits: Be mindful of the annual dollar limitations for HSA contributions. All contributions made to an employee’s HSA, whether by the employee, employer, or another entity, must be aggregated for these limits.

Nonforfeitable Contributions: Once made, matching HSA contributions are nonforfeitable. They cannot be subject to a vesting schedule or be returned to the employer if the employee terminates employment midyear.

Communicating the Plan to Employees

Effective communication is key to the success of your HSA matching program. Ensure that the details of the matching contributions are clearly outlined in the cafeteria plan document, summary plan description, and other employee communications, such as open enrollment materials.

Implementing matching HSA contributions through your company’s cafeteria plan can significantly enhance your employee benefits package. By understanding and complying with the relevant regulations, you can offer a valuable benefit that helps attract and retain top talent while providing employees with a tax-advantaged way to save for medical expenses.

For more information on setting up a compliant HSA matching program, reach out to Sales@NueSynergy.com.