Health Savings Accounts (HSAs) are not just for covering medical expenses—they can also be a powerful tool for long-term investment. Recently named as one of the Top HSA providers in 2024 by Morningstar, NueSynergy offers unique investment opportunities that can help you grow your savings while enjoying significant tax benefits. In this blog, we’ll explore how NueSynergy’s HSAs can be leveraged for investment purposes, providing a dual benefit of healthcare savings and wealth accumulation.

Tax Advantages of HSAs

One of the most compelling features of HSAs is their triple tax advantage:

Tax-deductible contributions: Contributions to an HSA are made with pre-tax dollars, reducing your taxable income.

Tax-free growth: Earnings from interest, dividends, and capital gains within the HSA are not taxed.

Tax-free withdrawals: Withdrawals for qualified medical expenses are tax-free.

These benefits make HSAs more advantageous than traditional retirement accounts like 401(k)s and IRAs.

Investing with NueSynergy’s HSAs

NueSynergy stands out for its investment-friendly features. Here are some key points to consider:

1. High-Quality Investment Options

NueSynergy offers an all-ETF lineup, which is the cheapest among its peers, with an average expense ratio of just 0.05%. This low-cost structure allows you to maximize your investment returns. Additionally, as stated in Morningstar, NueSynergy’s investment offerings include no Neutral- or Negative-rated funds, and 64% of its menu was Gold-rated as of August 2024. This high-quality selection ensures that your investments are in reliable and well-performing funds.

2. No Minimum Balance Requirements

NueSynergy does not require a minimum balance to start investing, making it accessible for all account holders. This flexibility allows you to begin investing as soon as you open your HSA, without having to wait until you accumulate a certain balance.

Strategies for Maximizing Investments with NueSynergy

To make the most of your HSA as an investment tool with NueSynergy, consider the following strategies:

1. Maximize Contributions

For 2025, the maximum HSA contribution is $4,300 for individuals and $8,550 for families. If you’re 55 or older, you can contribute an additional $1,000. Maximize your contributions each year to take full advantage of the tax benefits and growth potential.

2. Invest Aggressively Early On

If you’re young and healthy, consider investing aggressively in your HSA. With a longer time horizon, you can afford to take on more risk, which can lead to higher returns.

3. Use Other Funds for Medical Expenses

To allow your HSA investments to grow, try to cover current medical expenses out-of-pocket if possible. This way, your HSA can continue to grow tax-free, providing a larger nest egg for future healthcare costs or retirement.

NueSynergy’s Health Savings Accounts offer a unique opportunity to combine healthcare savings with robust investment potential. By understanding the tax advantages and investment opportunities NueSynergy provides, you can maximize your financial health and secure a more prosperous future.

NueSynergy has earned its place among the top HSA providers by offering a range of features that cater to the needs of its users:

Investment Options: NueSynergy was recognized for its extensive variety of value-based investment options, with the majority consisting of gold rated Morningstar funds.

Competitive Interest Rates: Account holders benefit from competitive interest rates on their deposits, ensuring their money grows even as they use it for medical expenses.

User-Friendly Platform: The intuitive platform makes it easy to manage accounts, track expenses, and make informed investment decisions.

National HSA Day

Earlier this week, we celebrated National HSA Day, which recognizes the importance of Health Savings Accounts (HSAs), raising awareness about their benefits. HSAs can be used not only for immediate medical expenses but also as a strategic tool for retirement planning. By understanding and utilizing HSAs, individuals can take control of their healthcare finances and secure a healthier financial future.

As we celebrate National HSA Day, it’s the perfect time to explore the benefits of HSAs and consider why NueSynergy is a top choice for managing your healthcare savings. With its competitive interest rates and robust investment options, NueSynergy stands out as a leader in the industry. Take advantage of this day to learn more about HSAs and how they can benefit you and your family.

What is an HSA?

A Health Savings Account (HSA) is a tax-advantaged savings account designed to help individuals with high-deductible health plans (HDHPs) save for medical expenses. HSAs offer a triple tax benefit: contributions are tax-deductible, earnings grow tax-free, and withdrawals for qualified medical expenses are also tax-free. This makes HSAs a powerful tool for both current healthcare spending and long-term savings.

About NueSynergy

NueSynergy is known for industry-leading service, innovative technology, and excellence in providing full-service administration of consumer-driven and traditional account-based plans to employers of all sizes and sectors. NueSynergy offers a fully integrated suite of administration services, which include Health Savings Account (HSA), Health Reimbursement Arrangement (HRA), Flexible Spending Account (FSA), Lifestyle Savings Account (LSA), and COBRAcare+ administration as well as SpouseSaver Incentive Account, Combined Billing, Direct Billing, and Specialty Solutions. For more information, visit https://nuesynergy.com/

About Morningstar

Morningstar is a leading provider of independent investment research and insights. The company offers a wide range of products and services for individual investors, financial advisors, asset managers, and institutional investors. Morningstar provides data and research on various investment offerings, including mutual funds, ETFs, stocks, and bonds. Additionally, they offer investment management services through their subsidiaries, managing approximately $286 billion in assets as of December 31, 2023. Morningstar operates in 32 countries, empowering investor success globally.

As the back-to-school season approaches, parents and students are preparing for the new academic year. Beyond the usual school supplies, there are many health-related items eligible for purchase using your Flexible Spending Account (FSA) or Health Savings Account (HSA). These tax-advantaged accounts can help you save money on essential health products that support your child’s well-being throughout the school year.

1. First Aid Supplies

Accidents happen, especially on the playground or during sports activities. Stock up on first aid essentials like bandages, antiseptic wipes, and cold packs. These items are crucial for handling minor injuries promptly.

If your child uses contact lenses, ensuring they have the right contact solution is essential for maintaining eye health and comfort. Both prescription glasses and contact lenses are eligible expenses, so make sure they have a clear view of the blackboard and their textbooks.

Managing acne is crucial for your child’s confidence and skin health. Various acne treatments, including creams, gels, and cleansers, are eligible for purchase with your FSA or HSA.

Protecting your child’s skin from harmful UV rays is important year-round. Ensure you have an adequate supply of sunscreen, particularly if your child spends a lot of time outdoors.

Leveraging your FSA or HSA for back-to-school shopping not only ensures your child is well-prepared but also helps you save on essential health-related products. By planning ahead and purchasing these eligible items, you can take advantage of the tax benefits these accounts offer.

For a complete list of eligible FSA and HSA back-to-school items click here.

For more information on all FSA and HSA eligible items, visit the FSA Store.

As a plan sponsor of a self-insured health plan, it’s crucial to maintain accurate records and ensure that all enrolled employees meet the eligibility criteria. However, situations can arise where outdated information leads to ineligible employees being enrolled in the health plan. If you’ve discovered that employees working 25 hours per week have been enrolled based on old handbook information, while your plan documents and Summary Plan Description (SPD) correctly state a 30-hour threshold, swift and strategic action is required.

Immediate Steps for Plan Sponsors

Upon discovering such errors, you must act promptly to minimize complications and potential liabilities. Here are two primary options to consider:

Allow Ineligible Employees to Remain Enrolled:

Fairness Consideration: Allowing employees to remain in the plan for the rest of the plan year can be seen as fair, especially if they relied on the outdated handbook information. This approach reduces the risk of employees seeking equitable relief due to miscommunication.

Stop-Loss Insurance Risk: Check with your stop-loss insurer before proceeding. Stop-loss coverage typically adheres to the terms in the plan document, not ancillary documents like handbooks. Without insurer approval, claims from these employees might not be covered under your stop-loss policy.

Remove Ineligible Employees from the Plan:

Consistency with Plan Terms: Removing these employees aligns with the plan document and SPD, mitigating the risk of significant uncovered claims under your stop-loss policy.

Prospective Removal: Ensure the removal is prospective, not retroactive, to avoid the impermissible “rescission” of coverage. Retroactive removal could lead to significant legal and ethical issues.

Equitable Relief Risk: Be aware of the potential for employees to claim equitable relief for lost benefits due to reliance on the outdated handbook.

Ensuring Compliance and Fair Treatment

Consistency is key in handling such situations. Treat all similarly situated employees alike to avoid claims of discrimination under various laws. Disparate treatment can lead to claims of discrimination based on sex, race, age, or health status. Additionally, adhere to the nondiscrimination rules under Code § 105(h) for self-insured health plans.

Discovering ineligible employees enrolled in your health plan requires careful consideration and prompt action. Whether you decide to keep the employees enrolled for the remainder of the plan year or remove them, ensure that your actions are consistent with plan terms and fair to all employees. By addressing the issue swiftly and consulting with your stop-loss insurer, you can mitigate potential risks and maintain the integrity of your health plan.

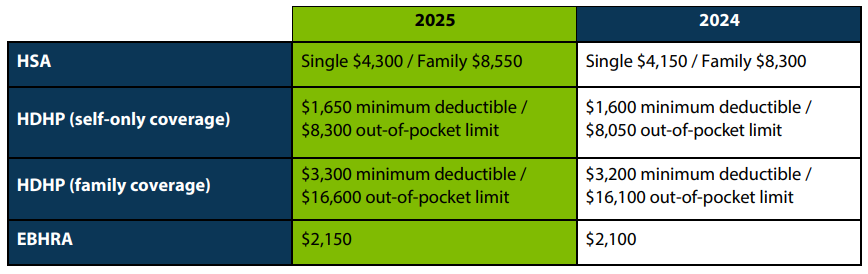

The IRS recently announced the 2025 limits for Health Savings Accounts (HSAs) and High Deductible Health Plans (HDHPs). HSA contribution and plan limits will increase to $4,300 for individual coverage and $8,550 for family coverage. Changes to these limits will take effect January 2025.

HSAs are tax-exempt accounts that help people save money for eligible medical expenses. To qualify for an HSA, the policyholder must be enrolled in an HSA-qualified high-deductible health plan, must not be covered by other non-HDHP health insurance or Medicare, and cannot be claimed as a dependent on a tax return.