Adding a High-Deductible Health Plan (HDHP) paired with a Health Savings Account (HSA) is a popular way for employers to enhance their benefits offerings. One common question that arises during implementation is whether employers must verify each employee’s eligibility before making HSA contributions.

Here’s what HR teams and employers need to know.

Are Employers Required to Verify HSA Eligibility?

The short answer: No—employers are not required to verify an employee’s HSA eligibility.

Instead, the responsibility largely falls on the employee. According to IRS guidance and informal commentary, employees are primarily accountable for ensuring they meet the eligibility criteria to contribute to an HSA.

✅What Employers Are Responsible For

While employers are not responsible for full eligibility verification, they must determine a few key factors:

Health Plan Coverage Employers must identify whether the employee is enrolled in:

A qualifying HDHP, or

A non-HDHP plan (such as a general-purpose FSA or HRA offered by the employer)

Employee Age This determines eligibility for catch-up contributions (age 55+). Employers may rely on employee-provided information for birthdates.

The “Reasonable Belief” Standard

Even though verification isn’t mandatory, employers must have a reasonable belief that their HSA contributions are excludable from the employee’s taxable income.

If this standard isn’t met:

Contributions may become subject to federal employment taxes

This includes income tax withholding and FICA

👉 In other words, while you don’t need to audit employees, you shouldn’t ignore obvious eligibility concerns either.

What Makes an Employee HSA-Eligible?

Employees enrolled in your HDHP are generally eligible to receive HSA contributions if they:

✅ Have no disqualifying coverage (e.g., coverage under a spouse’s non-HDHP plan)

✅ Are not enrolled in Medicare

✅ Cannot be claimed as someone else’s tax dependent

These factors are often outside the employer’s visibility, which is why the responsibility rests with employees.

💡 Best Practices for Employers

Even though verification isn’t required, many employers take proactive steps to reduce risk and educate employees:

✔️ 1. Use Employee Certifications

Ask employees to confirm that they meet HSA eligibility criteria. This helps:

Prevent improper contributions

Increase employee awareness

✔️ 2. Provide Educational Resources

Offer:

Simple eligibility checklists

Decision tools

FAQs about HSAs

✔️ 3. Communicate Clearly

Explain that:

Eligibility is the employee’s responsibility

Incorrect contributions could result in tax consequences

📊 Why This Matters

Making HSA contributions for ineligible employees can lead to:

Unexpected tax liabilities

Payroll correction issues

Administrative headaches

Taking light precautionary steps—like certifications and education—can go a long way in avoiding these problems.

✔️ Key Takeaway

Employers do not need to verify HSA eligibility, but they must:

Ensure proper plan classification

Maintain a reasonable belief in tax exclusion

A balanced approach—combining minimal oversight with employee education—helps protect both the organization and its workforce.

If you’re planning to roll out an HDHP/HSA option, putting a simple process in place now can save time, cost, and confusion later.

If your employer offers help paying for education, it’s often through something called a Qualified Educational Assistance Program (QEAP). But what exactly does that mean—and what can you have reimbursed?

This guide breaks it down in simple terms so you can take full advantage of this valuable benefit.

What Is a Qualified Educational Assistance Program?

A Qualified Educational Assistance Program (QEAP) is an employer-sponsored benefit that helps pay for your education. Under IRS rules, it allows your employer to provide tax-free education assistance up to $5,250 per year.

✅ What makes it special?

You don’t pay federal income tax on eligible reimbursements (up to the limit)

Your employer can cover a wide range of learning opportunities

The education does not have to be job-related in most cases

What Expenses Can Be Reimbursed?

Depending on your company’s plan, a QEAP may cover:

Tuition and required fees

Books and course materials

In some cases, student loan payments

✅ The education does not have to be related to your current job, so you have flexibility to pursue different interests or career goals.

What Is Not Covered?

Some expenses are not eligible, including:

Meals, transportation, and lodging

Most hobby or recreational courses (unless required for a degree or job-related)

Supplies or equipment you can keep after completing the course (except textbooks)

Important Rules to Remember

Up to $5,250 per year is tax-free

Your employer may set requirements, such as:

Getting course approval in advance

Attending approved schools or programs

Earning a minimum grade

Bottom Line

A QEAP is a valuable benefit that helps you save on education costs while growing your skills. To make the most of it, review your company’s specific rules and get any needed approvals before enrolling.

June is Men’s Health Month—a time dedicated to raising awareness about preventable health issues and encouraging men to take proactive steps toward living healthier, longer lives. From routine screenings to mental health support, prioritizing wellness is essential. The good news? If you have a Flexible Spending Account (FSA), Health Savings Account (HSA), or Health Reimbursement Arrangement (HRA), you may already have tax-advantaged funds available to support your health journey.

Why Men’s Health Matters

Many common health risks for men—such as heart disease, high blood pressure, and certain cancers—can often be prevented or managed with early detection and lifestyle adjustments. However, studies consistently show that men are less likely than women to visit a doctor regularly or seek preventive care.

Men’s Health Month serves as a reminder to:

Schedule annual physical exams

Monitor key health metrics (blood pressure, cholesterol, glucose)

Address mental health concerns

Stay active and maintain a balanced diet

What Are FSA, HSA, and HRA Accounts?

Before diving into how these accounts can support men’s wellness, let’s break down what they are:

FSA (Flexible Spending Account): Employer-sponsored account that allows you to set aside pre-tax dollars for eligible medical expenses.

HSA (Health Savings Account): A tax-advantaged savings account available with high-deductible health plans; funds roll over year to year.

HRA (Health Reimbursement Arrangement): Employer-funded account used to reimburse qualified healthcare expenses.

Each account helps you save money while investing in your health.

Eligible Men’s Health Expenses You Can Cover

Your FSA, HSA, or HRA can be used for a variety of services and products that directly support men’s health.

Preventive Care & Screenings

Early detection saves lives—and these accounts can help cover:

Annual physical exams

Prostate cancer screenings

Colonoscopies

Blood pressure monitoring

Fitness & Lifestyle Support

While gym memberships themselves may not always qualify, certain items and programs may be eligible with medical necessity:

Weight-loss programs prescribed by a doctor

Smoking cessation programs

Nutritional counseling

Mental Health Services

Mental wellness is just as important as physical health. Eligible expenses may include:

Therapy or counseling sessions

Psychiatric services

Telehealth mental health visits

Everyday Health Products

You can also use your funds for:

Over-the-counter medications

Pain relievers

First-aid supplies

Sunscreen (SPF 15+)

Pro Tips for Maximizing Your Benefits

Make the most of your FSA, HSA, or HRA this Men’s Health Month with these simple tips:

✅ Schedule checkups early: Don’t wait until the end of the year—stay proactive. ✅ Track your expenses: Use your plan’s portal or app to monitor spending and receipts. ✅ Know your deadlines: FSAs often have “use-it-or-lose-it” rules. ✅ Check eligibility: Not all items qualify—review your plan or use an eligibility tool.

Take Charge of Your Health Today

Men’s Health Month is the perfect opportunity to prioritize your well-being—and your FSA, HSA, or HRA makes it easier and more affordable to do so. Whether it’s scheduling a routine screening, addressing stress, or investing in healthier habits, every step counts.

Your health is one of your most valuable assets—make the most of it.

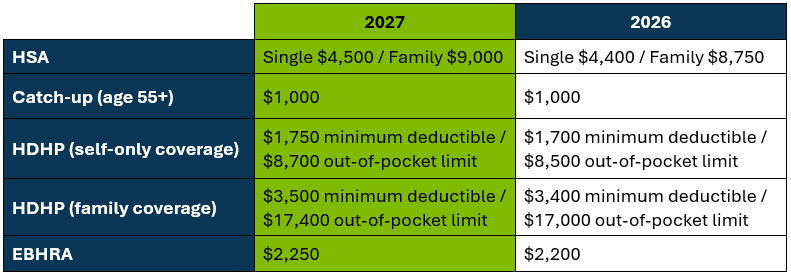

The IRS has released the 2027 cost-of-living adjusted limits for Health Savings Accounts (HSAs) and High-Deductible Health Plans (HDHPs). Changes to these limits will take effect January 2027.

HSA Contribution Limits: The 2027 limit is $4,500 for individuals with self-only HDHP (up from $4,400 in 2026), and $9,000 for individuals with family HDHP coverage (up from $8,750 in 2026).

HSA Catch-Up Contribution: Individuals age 55 and older can contribute an additional $1,000 catch-up contribution annually. This amount remains unchanged for 2027.

HDHP Minimum Deductibles: The 2027 deductible is $1,750 for self only HDHP coverage (up from $1,700 in 2026), and $3,500 for family HDHP coverage (up from $3,400 in 2026).

HDHP Out-of-Pocket Maximums: The 2027 limit, including deductibles, copayments, and coinsurance, is $8,700 for self-only HDHP coverage (up from $8,500 in 2026), and $17,400 for family HDHP coverage (up from $17,000 in 2026).

EBHRA (Expected Benefit HRA) Contribution Limit: The 2027 maximum amount is $2,250 (up from $2,200 in 2026).

The short answer is no, you don’t file a Form 5500 for the cafeteria plan itself. But you might have to file one for the specific benefits inside it.

Think of a cafeteria plan (a Section 125 plan) like a shopping cart. The cart itself doesn’t trigger tax or reporting rules—but the items you put inside the cart might.

Here is how it works in three simple steps.

1. The “Shopping Cart” is Free (The IRS Rule)

A cafeteria plan is just a tax structure that lets employees buy benefits using pre-tax dollars. The IRS suspended the rule requiring a Form 5500 for the plan structure itself. So, you can cross the cafeteria plan itself off your filing list.

2. Check the “Items” Inside (The DOL Rule)

While the cart is exempt, the Department of Labor (DOL) cares about the actual benefits you are funding through it. These are called component plans.

You need to look at each individual benefit you offer pre-tax, such as:

Your group health insurance plan

A Health FSA (Flexible Spending Account)

Dental or vision insurance

3. The “Under 100” Rule (Who actually has to file?)

Most small businesses don’t have to file a Form 5500 because of a size exemption.

If you have FEWER than 100 participants: You usually do not have to file a Form 5500 for your benefits, as long as they are paid out of the company’s general bank account or through an insurance company.

If you have 100 or MORE participants: You must file a Form 5500 for that specific benefit (like your main health insurance plan).

> Note: “Participants” usually means employees signed up for the plan on the very first day of the plan year. You do not count their dependents (spouses or kids).

Summary Checklist for HR

Count your heads: Did any of your pre-tax benefits have 100 or more employees enrolled on day one of the plan year?

If NO: You are likely exempt from filing a Form 5500 entirely.

If YES: You must file a Form 5500 for that specific benefit plan. You’ll do this electronically using the government’s online system, called EFAST2.

Pro-Tip: If you do have over 100 employees, ask your insurance broker about a “Wrap Document.” This combines all your different benefits into one single bundle so you only have to file a single Form 5500 instead of three or four separate ones.