The holiday season is a time for celebration, but it can also bring its share of stress—especially when it comes to travel. To help you stay healthy and prepared, here are the top five FSA (Flexible Spending Account) and HSA (Health Savings Account) eligible items you should pack for your holiday adventures.

A well-stocked first aid kit is essential for any traveler. Look for kits that include band-aids, antiseptic wipes, and other basic supplies. Many first aid kits are FSA/HSA eligible, ensuring you’re ready for minor injuries or ailments while on the road.

Protecting your skin is crucial, even in winter. Sunscreen is often FSA/HSA eligible and perfect for those sunny holiday destinations. Choose a broad-spectrum SPF to shield your skin from harmful UV rays, whether you’re skiing or lounging by the beach.

Over-the-counter pain relievers like ibuprofen or acetaminophen are must-haves for any trip. These items are typically FSA/HSA eligible and can help you manage headaches, muscle aches, or any discomfort that might arise during your travels, ensuring you can enjoy your holiday without interruptions.

A digital thermometer is a handy tool to have, especially during flu season. Keeping track of your health is easier with this essential item. Many thermometers qualify for FSA/HSA reimbursement, making it a smart addition to your travel kit.

If you suffer from allergies, packing your allergy medications is essential. Antihistamines and nasal sprays are often FSA/HSA eligible and can help you manage symptoms while traveling. Whether it’s pollen, pet dander, or dust, having your allergy meds on hand will keep you comfortable and ready to enjoy the festivities.

Traveling during the holiday season doesn’t have to be stressful, especially when you’re prepared. By packing these five FSA/HSA eligible items, you can ensure a healthier, more enjoyable trip. Remember, taking care of your health is the best gift you can give yourself this holiday season. Safe travels!

For a full list of FSA/HSA eligible items, click here.

QUESTION: Our company sponsors a group health plan that offers coverage to eligible employees and dependent children. We understand that we must make coverage available until a child is age 26. At what point during the month of the child’s 26th birthday is it permissible for our plan to terminate coverage for the child?

ANSWER: Group health plans that offer dependent coverage are required to continue making coverage available for an employee’s child until the child’s 26th birthday—regardless of the child’s residency, financial dependence, student status, employment, or other factors. Your plan will satisfy the dependent coverage requirement if coverage is provided until a child attains 26 years of age. As an example, assume an employee’s child’s birthday is July 17. The plan need only offer coverage for the child through the day before his or her 26th birthday—i.e., July 16.

Keep in mind, however, that if your company is an applicable large employer (i.e., if you employed an average of 50 or more full-time employees (or equivalents) in the preceding year), you could face potential employer shared responsibility penalties if you do not offer coverage to an employee’s child through the last day of the month containing the child’s 26th birthday. Applicable large employers may be subject to these penalties if they fail to offer adequate health insurance to full-time employees “and their dependents.” For this purpose, “dependents” means an employee’s children, but excluding stepchildren and foster children, who are under 26 years of age. Regulations implementing the penalties specifically provide that a child is a dependent for the entire calendar month during which he or she attains age 26. Thus, in the example above, coverage must be offered through July 31 to avoid potential penalties. Absent information to the contrary, employers may rely on employees’ representations concerning the identity and ages of the employees’ children.

QUESTION: Our company’s major medical plan offers a choice of self-only or family coverage. Dependent coverage is provided under the family coverage option for participants’ children who have not yet reached age 26. May our plan impose an additional premium surcharge for children who are older than age 18?

ANSWER: A premium surcharge for coverage of children over age 18 is not permitted because your plan would be impermissibly varying the terms for dependent coverage of children based on age. The Affordable Care Act (ACA) requires group health plans that provide dependent coverage of children to make such coverage available for a child until age 26. In addition, the terms and conditions under which dependent coverage is provided for children cannot vary based on age, except for children who are age 26 or older. This rule is known as the “uniformity requirement.”

Although your plan may not impose a surcharge for these children, revising or repricing the plan’s coverage tiers without making the structure age-based may allow your company to accomplish the same financial goals. For example, a plan design in which the cost of coverage increases for tiers with more covered individuals would not violate the ACA’s age 26 mandate, so long as the increase applies without regard to the age of any child. Although you did not specify whether your plan is grandfathered, it is important to note that changing coverage tiers can adversely affect a plan’s status as a grandfathered plan.

QUESTION: As required, our company’s group health plan has extended COBRA election and payment deadlines due to the COVID-19 emergency. How do we handle these deadlines once the outbreak period ends?

ANSWER: As you note, certain COBRA deadlines have been extended—but for no longer than one year—by disregarding (tolling) the COVID-19 “outbreak period,” which began March 1, 2020, and is set to end on July 10, 2023. Agency guidance issued in March 2023 provided examples illustrating the effect of the outbreak period’s end on COBRA election and premium payment deadlines:

Electing COBRA. If a participant experiences a qualifying event and is provided a COBRA election notice on or before July 10, 2023, the individual’s 60-day period to elect COBRA begins to run on July 10, 2023 (making the deadline September 8, 2023). If the qualifying event occurs after July 10, 2023, there is no extension, and the 60-day period is measured from the date the COBRA election notice is provided. Although not expressly addressed, it appears that if a qualifying event occurs on or before July 10, 2023, and the COBRA election notice is provided after that date, the COBRA election deadline would be measured from the provision of the notice.

Paying COBRA Premiums. The guidance provides an example of a COBRA election made on October 15, 2022, retroactive to October 1, 2022. The initial COBRA payment, covering premiums from October 2022 through July 2023 must be made no later than 45 days after July 10, 2023 (i.e., August 24, 2023), with subsequent payments due according to the regular COBRA timeline (the first day of each month of coverage, with a 30-day grace period).

In addition to COBRA deadlines, the end of the outbreak period also affects certain other plan-related deadlines, including those for claims and appeals and HIPAA special enrollments. The agencies have noted that nothing in the Code or ERISA prevents group health plans from continuing to extend deadlines and have encouraged plans to do so—at least for a while—as the outbreak period comes to an end. Keep in mind, however, that any extension beyond what is required should be cleared with plan insurers and stop-loss insurers, as applicable.

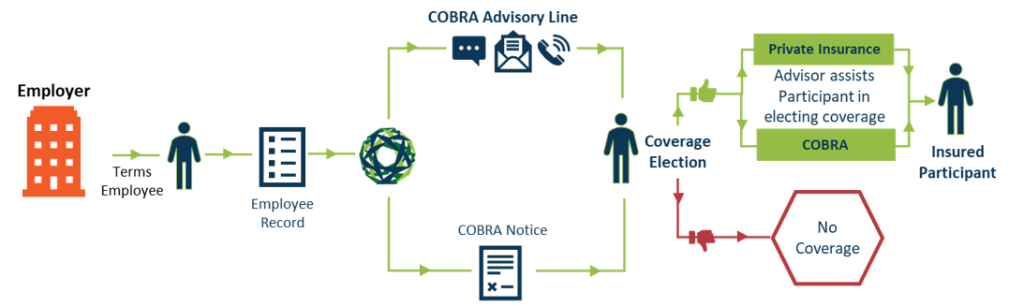

Our new enhanced Cobra solution. COBRAcare+ is a complimentary, cost-saving service offered exclusively by NueSynergy. Participants will get improved engagement through our COBRAcare+ advisory line where they will be guided by a licensed agent to compare COBRA benefits vs. alternative indiviudal health coverage options including subsidies.