In response to the end of the COVID-19 emergency, the IRS has issued a notice modifying its 2020 guidance regarding the COVID-19 testing and treatment benefits that can be provided by a high-deductible health plan (HDHP). Under the 2020 guidance, HDHPs can provide those benefits without a deductible or with a deductible below the applicable HDHP minimum deductible (self-only or family), thereby allowing individuals to receive coverage under HDHPs that provide such benefits on a no- or low-deductible basis without any adverse effect on HSA eligibility. Agency FAQs issued earlier this year indicated that the 2020 guidance would apply until further guidance was issued. This latest notice provides that, due to the end of the COVID-19 emergency, the relief described in the 2020 guidance is no longer needed and will apply only for plan years ending on or before December 31, 2024.

The notice also addresses the status of certain items and services as preventive care under the Code’s HSA eligibility rules. According to the notice, the preventive care safe harbor under those rules does not include COVID-19 screening (i.e., testing), effective as of the notice’s publication date. The notice acknowledges that the preventive care safe harbor includes screening services for certain infectious diseases but also observes that screenings for “common and episodic illnesses, such as the flu” are not included and concludes that COVID-19 differs from the types of diseases on the list. The notice further provides that—consistent with recent agency FAQs regarding the impact of the trial court’s decision in the Braidwood case—items and services recommended with an “A” or “B” rating by the United States Preventive Services Task Force (USPSTF) on or after March 23, 2010, are treated as preventive care under the HSA eligibility rules, whether or not they must be covered without cost sharing under the preventive services mandate. Thus, if the USPSTF were to recommend COVID-19 testing with an “A” or “B” rating, then that testing would be treated as preventive care under the HSA eligibility rules, regardless of whether coverage without cost-sharing is required under the preventive services mandate.

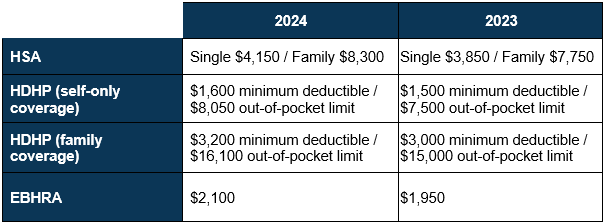

The IRS has just released the 2024 limits for Health Savings Accounts (HSAs) and High Deductible Health Plans (HDHPs). HSA contribution and plan limits will increase to $4,150 for individual coverage and $8,300 for family coverage. Changes to these limits will take effect January 2024.

HSAs are tax-exempt accounts that help people save money for eligible medical expenses. To qualify for an HSA, the policyholder must be enrolled in an HSA-qualified high-deductible health plan, must not be covered by other non-HDHP health insurance or Medicare, and cannot be claimed as a dependent on a tax return.

This week, the IRS released 2023 cost-of-living adjusted limits for health savings accounts (HSAs), high-deductible health plans (HDHPs), and excepted benefit health reimbursement arrangements (EBHRAs). All of these limits have increased from 2022. Everything you need to know about each limit increase is stated in our press release, which is down below.

Congress has passed, and the President has signed, omnibus spending legislation that (among other things) temporarily exempts telehealth and other remote care services from certain restrictions affecting health savings account (HSA) eligibility. By way of background, tax-advantaged contributions generally cannot be made to an HSA unless the account holder is covered by a qualifying high-deductible health plan (HDHP) and does not have disqualifying non-HDHP coverage.

In the Coronavirus Aid, Relief, and Economic Security Act (CARES Act), Congress created exceptions to those rules to facilitate the use of telehealth during the COVID pandemic, but those exceptions applied only to plan years beginning on or before December 31, 2021. The new legislation—the Consolidated Appropriations Act, 2022—restores these exceptions for the last nine months of 2022.

The new legislation amends two key provisions in the Code 223 rules for HSAs. First, it provides that telehealth and other remote care services will be considered disregarded coverage—and thus will not cause a loss of HSA eligibility—during the months beginning after March 31, 2022, and before January 1, 2023. Second, during that nine-month period, plans may provide coverage for telehealth and other remote care services before the HDHP minimum deductible is satisfied without losing their HDHP status. Both amendments apply to the stated months without regard to the HDHP’s plan year. The relief does not apply for the first three months of 2022 so some plans (e.g., calendar-year plans) must still apply their minimum deductible to telehealth and other remote care services during those months. [EBIA Comment: Plans with 2021 plan years that started on or after April 1, 2021, should be unaffected by the three-month gap that affects other plans, because their CARES Act relief will not expire until those plan years end.]

EBIA Comment: HDHPs are not required to waive their minimum deductible for telehealth and other remote services during the additional relief period, so some plan sponsors may conclude that a midyear change to take advantage of the restored exceptions is too difficult to communicate and administer, and not worth the effort. Other plan sponsors, those who assumed Congress would extend the CARES Act relief without a gap and covered telehealth during the first three months of 2022 without applying the minimum deductible, may have a different problem: determining whether their plans can and should apply the minimum deductible to telehealth and other remote services retroactively to the gap period. Some covered individuals may be able to avoid the adverse HSA-eligibility consequences of their plan’s failure to satisfy the minimum deductible requirement during the first three months of 2022 by using the full contribution rule, which allows a full year’s worth of HSA contributions to be made by someone who is HSA-eligible for only a portion of the year. (This rule is also sometimes referred to as the “last-month rule” or the “no-proration rule.”) But that rule may not be available to all affected plan participants because some may not be HSA-eligible on December 1, 2022, and some may not remain HSA-eligible throughout the 13-month testing period beginning on that date.