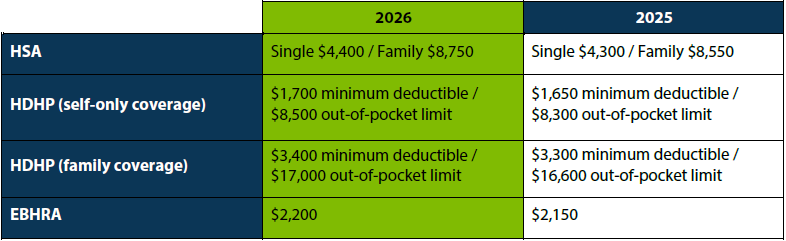

The IRS recently announced the 2026 limits for Health Savings Accounts (HSAs) and High Deductible Health Plans (HDHPs). HSA contribution and plan limits will increase to $4,400 for individual coverage and $8,750 for family coverage. Changes to these limits will take effect January 2026.

HSAs are tax-exempt accounts that help people save money for eligible medical expenses. To qualify for an HSA, the policyholder must be enrolled in an HSA-qualified high-deductible health plan, must not be covered by other non-HDHP health insurance or Medicare, and cannot be claimed as a dependent on a tax return.

Health Savings Accounts (HSAs) are a valuable tool for managing healthcare expenses, especially for those enrolled in high-deductible health plans (HDHPs). However, understanding the contribution limits can be tricky, particularly for married couples with self-only HDHP coverage. In this post, we’ll clarify whether spouses with self-only HDHP coverage can share their HSA contribution limits and provide insights into maximizing their contributions.

HSA Contribution Limits

For 2025, the HSA contribution limits are as follows:

Self-Only HDHP Coverage: $4,300

Family HDHP Coverage: $8,550

Additionally, individuals aged 55 or older can make a “catch-up” contribution of up to $1,000 to their HSA.

Special Rule for Married Individuals

When at least one spouse has family HDHP coverage, a special rule allows the spouses to share the higher family contribution limit. Either spouse’s HSA can receive contributions up to the family maximum, but their combined contributions cannot exceed the family limit. It’s important to note that HSAs are individual accounts, and married couples cannot maintain a joint HSA.

Scenario: Both Spouses Have Self-Only Coverage

In the situation where both spouses have self-only HDHP coverage, the special rule for married individuals does not apply. Each spouse’s contributions will be subject to the self-only limit, including any catch-up contributions if they meet the age requirement. One spouse cannot increase the other spouse’s maximum HSA contributions by contributing less.

Maximizing Contributions

If both spouses with self-only coverage each maintain HSAs and contribute the maximum amount, their aggregate contributions will be slightly more than the family limit ($8,600 versus $8,550). However, they lose the flexibility to place a disproportionate amount of the contribution into one spouse’s HSA. To maximize their aggregate contribution, married couples should:

Maintain two HSAs.

Maximize contributions to each HSA.

Considerations for Choosing Coverage

When deciding whether to elect self-only HDHP coverage from their respective employers or family HDHP coverage from one employer, married couples should consider various factors, including:

Premium costs

Provider networks

Deductible and other cost-sharing amounts

Any spousal surcharges

Understanding HSA contribution limits and rules is crucial for married couples with self-only HDHP coverage. By maintaining individual HSAs and maximizing contributions, they can effectively manage their healthcare expenses. Always consider the broader implications of your HDHP coverage choices to ensure you make the best decision for your financial and healthcare needs.

QUESTION: We are planning to add an HDHP and to make company contributions to employees’ HSAs. We have been told that an HSA contribution program—unlike the HDHP coverage—would not be subject to ERISA. Is that always true, or are there circumstances in which ERISA might apply?

ANSWER: Employer-facilitated HSA contribution programs generally are not subject to ERISA. Even though HSA funds may be intended to provide medical care, HSAs are viewed as personal accounts that are not ERISA-covered welfare benefit plans, so long as employee participation is completely voluntary and the employer’s involvement is limited. However, there are ways in which an HSA contribution program could become subject to ERISA. Those ERISA triggers should be avoided because ERISA’s compliance obligations were not crafted with HSAs in mind, and it is not clear how and whether all of ERISA’s requirements could be satisfied by an HSA program.

The DOL has established two safe harbors from ERISA coverage that may apply to workplace HSA programs. One, the voluntary plan safe harbor for group or group-type insurance programs, does not allow employer contributions, so for your purposes, we will focus instead on the HSA-specific safe harbor, which allows employer contributions. Under that safe harbor, employer contributions will not result in ERISA’s application if all of the following requirements are met:

Voluntary Employee Contributions. An employer using the safe harbor can unilaterally establish HSAs for employees and deposit employer funds into those accounts. But any contributions made by employees, including salary reduction contributions, must be voluntary.

Portable Funds. An employer’s program may limit forwarding of HSA contributions to a single HSA provider without triggering ERISA. But the employer cannot limit what happens after that initial deposit; employees must be able to move funds to another HSA if they desire.

Unrestricted Use of Funds. Some employers may wish to impose conditions on how HSA funds are used, such as a requirement that funds be used only for qualified medical expenses. Any such restrictions, however, will cause the arrangement to fall outside the safe harbor.

No Employer Influence. When selecting an HSA provider, employers may choose trustees or custodians that offer only a limited selection of investment options or options replicating those available under the employer’s 401(k) plan. Generally, however, the employer cannot make or attempt to influence employees’ investment decisions.

Not Represented as an ERISA Plan. This requirement seems simple, but it is also easily violated. Participant communications must not represent the HSA program as part of an ERISA plan, or as an ERISA plan of its own, and should include appropriate disclaimers indicating that the HSA is not part of an ERISA plan. From a drafting perspective, the HSA provisions should not be included in an ERISA plan document. While bundling non-ERISA and ERISA benefits will normally not make the non-ERISA benefits subject to ERISA, careful drafting and communications are required to ensure that the HSA satisfies the safe harbor.

No Employer Compensation. The employer cannot receive any direct or indirect payment or compensation in connection with its employees’ HSAs. This rule precludes discounts on other products that the employer may purchase from the HSA vendor, and may raise questions in other situations (e.g., bundled arrangements). This prohibition does not preclude making HSA contributions through a cafeteria plan; the employment tax savings realized by the employer is not considered compensation for this purpose.

Failure to meet any one of these elements will cause the program to fall outside the safe harbor. Although a program involving employer actions or program rules not specifically authorized by the safe harbor might still avoid ERISA, any variations should be discussed in advance with counsel.

QUESTION: Our group health plan uses a copay accumulator program that does not count drug manufacturers’ financial assistance toward participants’ cost-sharing limits. We’ve heard that the agencies have restricted the use of these programs. Can we continue to exclude drug manufacturers’ coupons from cost-sharing?

ANSWER: The guidance in this area is in flux, and it is currently uncertain whether your plan may continue to exclude drug manufacturers’ coupons from cost-sharing using a “copay accumulator” program. To review, prescription drug manufacturers sometimes offer financial assistance to individuals for certain drugs to help defray costs that might otherwise be an impediment to obtaining the drug. Traditionally, this financial assistance reduced the participant’s cost-sharing under the plan. That is, the drug manufacturers would cover all or a portion of the participant’s deductible and copayment or other required cost-sharing under the plan (sometimes up to a specified dollar amount), and the manufacturers’ payments would count toward the participant’s satisfaction of the plan’s deductible and cost-sharing limit. Under a copay accumulator program, however, the drug manufacturers’ financial assistance does not count toward the plan’s deductible and cost-sharing limits. This can result in cost savings to the plan because more of the financial burden is placed on participants and drug manufacturers.

Plan sponsors must ensure that their copay accumulator programs do not violate the requirement that plans adhere to an established annual cost-sharing limit with respect to essential health benefits. Beginning in 2021, HHS regulations permitted, but did not require, plans and insurers to count drug manufacturers’ assistance toward the cost-sharing limit. However, in 2023 a court vacated the applicable provision in the regulations. This effectively revives a potential conflict that the vacated regulations were intended to address. Earlier HHS guidance had stated that manufacturers’ assistance need not be counted toward a plan’s annual cost-sharing limit when a medically appropriate generic equivalent was available, which some stakeholders viewed as implying that manufacturers’ assistance must be counted absent a medically appropriate generic equivalent. However, this interpretation potentially conflicts with the rules for high-deductible health plans (HDHPs), under which only amounts actually paid by the individual (i.e., not manufacturers’ assistance) may be taken into account when determining whether the HDHP deductible is satisfied.

QUESTION: How does the general contribution limit for HSAs work? It is often stated as an annual limit, but isn’t it really monthly? Our company is thinking about changing to HDHP coverage that would allow our employees to make HSA contributions. If we decide to facilitate those HSA contributions or to make employer contributions, would we need to limit the amount of contributions made each month, or only annually?

ANSWER: The general contribution limit for HSAs is an annual limit determined by the number of months of HSA eligibility. The HSA of an individual who is HSA-eligible for the entire year can receive contributions (from any source) up to the full annual limit. If an individual is only HSA-eligible for a portion of the year, the annual limit is prorated based on the number of months of HSA eligibility. A special rule that can change this outcome is noted below.

For example, if Ana, a 40-year-old calendar-year taxpayer, is HSA-eligible for all of 2023 and has self-only HDHP coverage, her HSA can receive contributions of up to the maximum of $3,850 for 2023. (For coverage other than self-only coverage, the maximum for 2023 is $7,750.) If Ana were only HSA-eligible for April through September, however, her annual limit would be 6/12ths of the full annual limit, or $1,925. That $1,925 could be contributed in one month, or in any number of payments made on or after January 1, 2023, and on or before the filing due date (without extensions) for Ana’s 2023 federal tax return. Some or all of the permitted amount could be contributed during a month in which Ana is not HSA-eligible, based on her prior or anticipated months of HSA eligibility. (Of course, contributions could not be made until Ana’s HSA is established, if it wasn’t established by January 1st.) A similar proration rule applies to HSA catch-up contributions, which increase the general contribution limit for HSA-eligible individuals who have attained age 55 by the end of the taxable year. Thus, if Ana were at least age 55 by the end of 2023, and she were HSA-eligible for the entire year, her limit would be increased by $1,000. But if she were HSA-eligible for only 6 months of 2023, her catch-up contribution limit would be only $500.

Employers that facilitate employee contributions or make their own contributions to employees’ HSAs need not limit the amount actually contributed in each month, but they do have to track their employees’ HSA eligibility on a monthly basis so they can determine any prorated limit amount. Employers are only responsible for knowing how their own benefit programs affect HSA eligibility and whether an employee is eligible for catch-up contributions. They need not determine whether employees have disqualifying coverage from other sources or how much has been contributed to employees’ HSAs by other means.

As noted above, special contribution rules can apply when determining a particular employee’s limit. One of these is the “full contribution rule,” which allows calendar-year taxpayers to be treated as HSA-eligible for the entire year if they are HSA-eligible on December 1st, subject to certain conditions that include remaining HSA-eligible for at least a 13-month testing period. There is also a special rule for married individuals if either spouse has family HDHP coverage.