If your company sponsors a self-insured health plan, you might be wondering whether you still need to pay Patient-Centered Outcomes Research Institute (PCORI) fees. These fees, which fund research on patient-centered outcomes, have been a requirement for several years. However, there have been changes to the legislation that you should be aware of. In this post, we’ll clarify the current requirements for PCORI fees and what you need to do to stay compliant.

What Are PCORI Fees?

PCORI fees are paid by health insurers and sponsors of self-insured health plans. The funds collected are used to support research that helps patients, clinicians, purchasers, and policymakers make informed health decisions.

Legislative Background

Initially, PCORI fees were required for plan and policy years ending before October 1, 2019. For calendar-year plans, this meant that the 2018 plan year was supposed to be the last year for which these fees applied. However, budget legislation passed in 2019 reinstated the PCORI provision, extending the fee requirements through plan years ending before October 1, 2029.

Current Requirements

As of now, if your self-insured health plan’s policy year ends on December 31, 2024, you are required to pay the PCORI fee. This fee is considered an excise tax under the Internal Revenue Code and must be reported on IRS Form 720. Although Form 720 is filed quarterly for other federal excise taxes, the PCORI fee reporting and payment are only required annually. The deadline for filing Form 720 for the 2024 plan year is July 31, 2025.

Record-Keeping

The instructions for Form 720 advise taxpayers to keep their tax returns, records, and supporting documentation for at least four years from the latest of the date the tax became due or the date the tax was paid. This is crucial for ensuring compliance and being prepared for any potential audits.

Conclusion

In summary, PCORI fees are still required for self-insured health plans through plan years ending before October 1, 2029. Make sure to file IRS Form 720 by July 31, 2025, for the 2024 plan year, and keep all related documentation for at least four years. Staying informed and compliant will help your company avoid any penalties and contribute to valuable health outcomes research.

As the FSA grace period draws to a close on March 15, it’s crucial to make the most of your remaining funds. Flexible Spending Accounts (FSAs) offer a fantastic way to save on healthcare expenses, but any unused money will be forfeited if not spent by the deadline. To help you avoid losing your hard-earned dollars, here are five essential items you can purchase with your leftover FSA money:

1. Prescription Eyewear

Why not treat yourself to a stylish new pair of prescription glasses or contact lenses? Not only will you see better, but you’ll also have a chic accessory. Check out the options at the FSA Store.

2. Over-the-Counter Medications

Stock up on everyday essentials like pain relievers, allergy meds, and cold remedies. These are FSA-eligible and super handy to have around. You can find a wide selection at the FSA Store.

3. First Aid Supplies

Be prepared for minor injuries and emergencies by updating your first aid kit. Grab some bandages, antiseptic wipes, and gauze. Check out the FSA Store for all your first aid needs.

4. Health and Wellness Products

Consider investing in health and wellness products like heating pads, hot/cold packs, or even a new humidifier. These items are FSA-eligible and can help you stay comfortable and healthy. Explore the options at the FSA Store.

5. Sunscreen and Skincare Products

Protect your skin by investing in high-quality sunscreen and skincare products. Many of these items are FSA-eligible, making them a smart choice for using up your remaining funds. Check out the FSA Store for some great options.

Don’t let your FSA money go to waste! By purchasing these essential items, you can maximize your savings and ensure you’re well-prepared for the year ahead. Remember to check with your FSA provider for a complete list of eligible expenses and make your purchases before the grace period ends. For a full list of eligible FSA items click here.

The IRS has released the optional standard mileage rates for 2025, providing important updates for businesses, medical care, and charitable activities. Here’s what you need to know about the new rates and vehicle value limits.

2025 Standard Mileage Rates

Business Use: The standard mileage rate for business use of an automobile has increased to 70 cents per mile, up from 67 cents in 2024. This rate can be used instead of calculating actual expenses like depreciation, lease payments, and fuel costs.

Medical and Moving Use: The rate for using an automobile to obtain medical care or for moving expenses remains unchanged at 21 cents per mile. This rate applies to variable expenses only, such as gas and oil, and does not include fixed costs like depreciation and insurance.

Charitable Use: The rate for charitable use of an automobile remains at 14 cents per mile.

Understanding the Rates

The standard mileage rates offer a simplified method for taxpayers to deduct automobile expenses. For business use, the rate covers both fixed and variable costs, while for medical and moving purposes, only variable costs are deductible. Parking fees and tolls related to medical or moving expenses can be deducted separately.

Vehicle Value Limits

The IRS has also set the maximum vehicle values for 2025, which determine the applicability of certain valuation rules for employer-provided vehicles:

Cents-Per-Mile Rule: This rule values personal use of an employer-provided vehicle by multiplying the business standard mileage rate by the number of personal miles driven.

Fleet-Average Valuation Rule: Employers with a fleet of 20 or more vehicles can use an average annual lease value for each vehicle in the fleet.

For vehicles first made available for personal use in 2025, the maximum vehicle value under both rules is $61,200, down from $62,000 in 2024. This value also sets the maximum standard automobile cost for reimbursement allowances under a fixed and variable rate (FAVR) plan.

These updates from the IRS provide clarity and consistency for taxpayers planning their 2025 automobile expenses. By understanding and utilizing the new standard mileage rates and vehicle value limits, individuals and businesses can better manage their tax deductions and compliance.

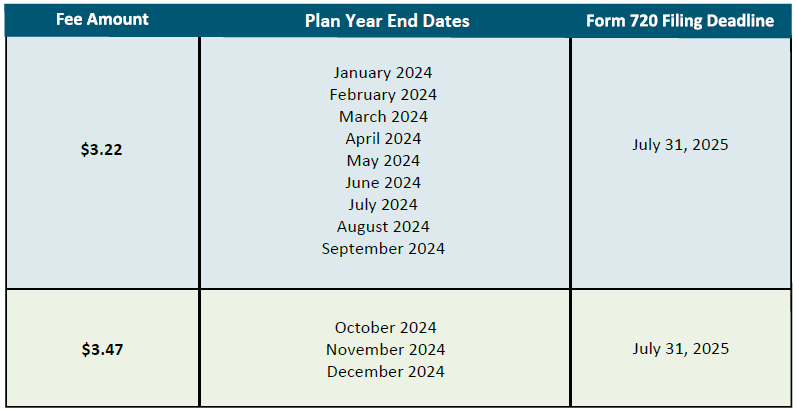

The IRS has released the 2025 Patient-Centered Outcomes Research (PCORI) fee amounts for health insurers and self-insured health plan sponsors. The PCORI fee is due on July 31, 2025. For plan and policy years ending between October 1, 2024, and October 1, 2025, the PCORI fee is $3.47 per covered life, up from $3.22 for the previous year. This is a $.25 increase from the amount in effect for plan and policy years ending on or after October 1, 2023, and before October 1, 2024.

PCORI fees are calculated by multiplying the applicable dollar amount for the year by the plans or policy’s average number of covered lives. These fees, established by the Affordable Care Act (ACA), fund clinical effectiveness research.

Below is the fee amount per plan year.

For more information on the upcoming PCORI fee deadline please refer to the IRS’ PCORI fee FAQ

The IRS announced the 2025 contribution limits for all Flexible Spending Account (FSA) plans. Below is an overview of the limit increases across all the types of FSAs except for Dependent Care FSAs, which remain the same at $5,000 per year.

Health Flexible Spending Account

The Health FSA, which provides employees the ability to set aside money on a pre-tax basis to pay for eligible medical, dental, and vision expenses will have an increase to its contribution maximum from $3,200 to $3,300 for 2025. The new contribution limit will also apply to the Limited Purpose FSA which reimburses eligible dental and vision expenses. Limited Purpose FSA limits will also increase from $3,200 to $3,300 for 2025.

Carryover Limit

The FSA Carryover limit provides employers the option to transfer a maximum amount of remaining FSA balances at a plan year’s end to carryover for use during the next plan year. This is available with Healthcare and Limited Purpose FSAs only. The carryover limits for this account will increase from $640 to $660 for 2025.

Commuter Benefits

Commuter Benefits help employees pay for certain parking, mass transit, and/or vanpooling expenses with pre-tax dollars. The contribution limits for this account will increase from $315 to $325 for 2025.

Adoption Assistance

The Adoption Assistance FSA helps employees pay eligible adoption expenses such as agency fees and court costs by contributing to the account with pre-tax money from their paycheck. The contribution limits for this account will increase from $16,810 to $17,280 for 2025.