Providing a Summary of Benefits and Coverage (SBC) that is culturally and linguistically appropriate is not just a good practice—it’s a legal requirement for many group health plans. Whether your plan is self-insured or fully insured, it’s essential to understand and comply with these regulations to avoid penalties and ensure your members can access and understand their benefits. In this blog post, we’ll break down what you need to know about furnishing the SBC in languages other than English.

Understanding the Requirement

The SBC must be presented in a “culturally and linguistically appropriate” manner. This requirement is part of a broader effort to ensure that individuals who are literate only in a non-English language can understand their health coverage options. The specific conditions under which this requirement is triggered are based on U.S. Census data.

When Does the Requirement Apply?

The requirement applies if your plan’s SBC is provided to individuals in any county where at least 10% of the population is literate only in the same non-English language. The Department of Health and Human Services (HHS) regularly updates a list of such counties and the languages that apply. As of January 1, 2025, a new list will come into effect, and it’s crucial for plan administrators to stay updated with these changes.

Compliance Steps for Group Health Plans

To comply with the “culturally and linguistically appropriate” requirement, follow these steps:

Identify Applicable Counties: Check the latest HHS list to see if any counties where your plan members reside meet the 10% threshold for non-English language literacy.

Provide Interpretive Services: In applicable counties, offer interpretive services in the relevant languages. This includes answering questions and providing assistance in the non-English language.

Include a One-Sentence Statement: On the SBC, include a one-sentence statement in the applicable non-English languages. This statement should clearly indicate how to access language services. It must be placed on the same page as the “Your Rights to Continue Coverage” and “Your Grievance and Appeals Rights” sections.

Offer Written Translations: Upon request, provide a written translation of the SBC in the applicable non-English language. The agencies have provided an SBC template that includes this one-sentence statement in all required languages for plan years beginning before 2025.

Stay Updated: Keep an eye on updates from the HHS, DOL, and IRS regarding additional translations and template updates. These resources will assist in maintaining compliance with the latest requirements.

Voluntary Compliance

Even if your plan does not operate in a county meeting the 10% threshold, you may choose to include the one-sentence statement in any non-English language. If you opt for this, ensure you are prepared to provide the necessary language services.

Differentiating SBC Requirements from ERISA

It’s important to note that the requirements for SBCs differ from ERISA’s rules on language assistance for Summary Plan Descriptions (SPDs) and Summary of Material Modifications (SMMs). Ensure you are familiar with both sets of regulations to avoid confusion and non-compliance.

Meeting the requirement for a culturally and linguistically appropriate SBC is vital for compliance and member satisfaction. By following the steps outlined above, your self-insured group health plan can ensure that all members understand their coverage options, regardless of their primary language. Stay informed, be proactive, and provide the necessary language services to comply with federal regulations and support your diverse member base.

Summer is right around the corner (June 21)! Whether you have plans to travel or are staying closer to home, your Flexible Spending Account can help you stock up on summer essentials without breaking the bank. Depending on your activity, your FSA can provide a variety of products! Below is a list of the top items to not only enhance your summer experience but also ensure your health and wellness.

Sunscreen

Sunscreen is a no-brainer when it comes to summer. With more time spent outdoors, protecting your skin from harmful UV rays is crucial. The last thing you want to worry about before heading to the beach or the pool is sunscreen. Buying sunscreen while on vacation can also be more expensive. Click here for all FSA eligible sunscreen bundle options.

First Aid

Whether you are dealing with mosquito bites, blisters from those long summer walks, or minor cuts and scrapes, accidents happen and being prepared is key. Click here for all FSA eligible medicine and treatment care.

Shoe Inserts

Comfortable footwear is essential for enjoying summer activities. A shoe insert can help reduce foot pain offering extra padding and improve blood circulation. Click here for all FSA eligible foot care options.

Eye Care

Protecting your eyes is just as important as protecting your skin. If you wear contact lenses, you want them to stay comfortable and clean. The FSA store offers a variety ofcontact lens solution and eye drops to make sure your eyes don’t get irritated throughout the days. Let’s not forget about the UV rays! The FSA store also offers sunglasses with or without prescription!

Your FSA is more than just a healthcare benefit; it’s a gateway to a healthier, more enjoyable summer. By investing in these FSA-eligible essentials, you’re not only making smart financial choices but also ensuring that you and your family can fully embrace all the joys that summer has to offer. So, dive into the season with confidence, knowing that you’re covered for every sunny day ahead.

For all FSA eligible items, or other HRA and HSA eligible items, click here.

Note: The products mentioned are based on the latest available information and are subject to change. Always check with your FSA provider for the most current eligibility list.

Understanding cafeteria plan election changes can be complex, especially when dealing with domestic partner relationships. Here’s what you need to know about whether such relationships qualify for election changes under cafeteria plan rules.

Domestic Partner Relationship and Election Changes

The commencement of a domestic partner relationship does not qualify as a “change in marital status” under cafeteria plan rules. Legal marital status changes include marriage, death of a spouse, divorce, legal separation, and annulment. While the list is not exhaustive, the IRS does not recognize the start or end of a domestic partner relationship as equivalent to these events.

Alternative Election Change Event: Change in Coverage Under Another Employer Plan

However, another permitted event, “change in coverage under another employer plan,” may allow for an election change. If your plan includes this provision, your employee can drop major medical coverage upon becoming covered under their partner’s employer plan. This event does not restrict changes to the plans maintained by the employer of a spouse or dependent but does not allow changes to health FSA elections.

Key Takeaways

Domestic Partner Relationship: Does not qualify as a change in marital status for election changes.

Change in Coverage: Employees can change their election if covered under a partner’s employer plan.

Documentation: Required to prove new coverage under the partner’s employer plan.

Plan Specifics: Check your specific cafeteria plan terms for detailed rules and procedures.

Conclusion

While domestic partner relationships don’t qualify for election changes under marital status rules, a change in coverage under another employer plan can allow adjustments. Always consult your cafeteria plan specifics and seek professional advice for compliance.

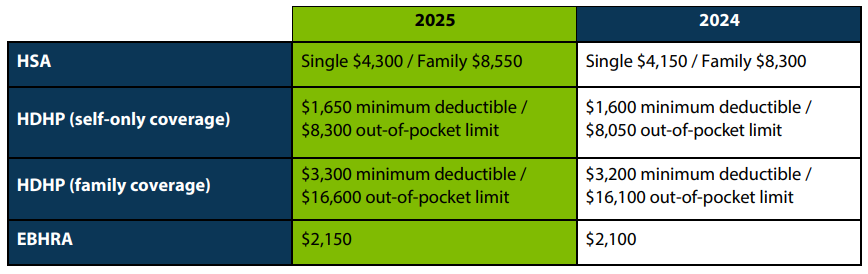

The IRS recently announced the 2025 limits for Health Savings Accounts (HSAs) and High Deductible Health Plans (HDHPs). HSA contribution and plan limits will increase to $4,300 for individual coverage and $8,550 for family coverage. Changes to these limits will take effect January 2025.

HSAs are tax-exempt accounts that help people save money for eligible medical expenses. To qualify for an HSA, the policyholder must be enrolled in an HSA-qualified high-deductible health plan, must not be covered by other non-HDHP health insurance or Medicare, and cannot be claimed as a dependent on a tax return.

Question: One of our employees would like to drop his DCAP election under our calendar-year cafeteria plan because a neighbor has offered to take care of his child at no cost. Can we allow this midyear election change?

Answer: Absolutely! However, there are specific conditions to consider. If your plan document has been drafted expansively, in line with IRS rules, midyear election changes due to changes in cost or coverage are permissible. Let’s break it down:

Broad Application of Rules:

The IRS rules apply broadly to DCAPs, allowing midyear election changes in various circumstances.

These circumstances include changes in care providers or adjustments in the cost of care.

Childcare Provider Switch:

A DCAP election change is permitted when a child transitions from a paid provider to free care (or no care, in the case of a “latchkey” child).

So, your employee’s situation aligns with this provision.

Other Allowable Changes:

Beyond provider switches, other scenarios also warrant a DCAP election change:

Adjustments in the hours for which care is provided.

Changes in the fee charged by a provider.

Relative Exception:

Be cautious: An election change isn’t allowed if the cost change is imposed by a care provider who is the employee’s relative (as defined by IRS rules).

Health FSAs vs. DCAPs:

Remember that the cost or coverage election change rules apply broadly to DCAPs but not to health flexible spending arrangements (health FSAs).

This distinction is essential for employers to navigate effectively.

As an employer, staying informed about DCAP rules ensures that you can accommodate midyear changes when necessary. By understanding the nuances, you can support your employees while maintaining compliance with IRS guidelines. If you have further questions, consult your tax or employee benefits advisors.

Remember, flexibility within the rules allows for better employee experiences and smoother transitions.

In the realm of cafeteria plans, health Flexible Spending Accounts (FSAs) and Dependent Care Assistance Programs (DCAPs) play a crucial role. However, the process of claim substantiation often raises questions among administrators. This blog post aims to shed light on the IRS rules regarding claim substantiation for health FSAs and DCAPs.

The Necessity of Claim Substantiation

According to IRS rules, all health FSA and DCAP claims must be substantiated. This substantiation requires information from an independent third party describing the service or product, the date of the service or sale, and the amount of the expense. These requirements are designed to ensure that health FSAs and DCAPs reimburse only legitimate claims.

The Role of Debit Card Programs

IRS rules regarding debit card programs also require that claims be substantiated and reviewed. However, certain categories of expenses are treated as automatically substantiated without any receipts or review beyond the swipe.

The Risk of Substantiation Shortcuts

Administrators might be tempted to engage in substantiation shortcuts such as reviewing only a percentage of claims (i.e., sampling) or automatically reimbursing claims that are below a “de minimis” dollar threshold or that appear to be from medical or dependent care providers. However, these actions could jeopardize the income exclusion that would otherwise apply to reimbursements from these arrangements under the Code. This could result in all reimbursements becoming taxable, not just those approved using the impermissible techniques.

The Consequences of Non-Compliance

If a health FSA or DCAP fails to comply with applicable substantiation requirements, all employees’ elections between taxable and nontaxable benefits under the entire cafeteria plan will result in gross income. A March 2023 IRS Chief Counsel’s office memorandum reconfirms the substantiation requirements for medical and dependent care expenses, as well as the prohibition and consequences of sampling and other substantiation shortcuts.

While the process of claim substantiation might seem daunting, it is a necessary step to ensure the legitimacy of claims under health FSAs and DCAPs. Administrators must adhere to IRS rules and avoid substantiation shortcuts to maintain the tax benefits of these programs.