In response to the end of the COVID-19 emergency, the IRS has issued a notice modifying its 2020 guidance regarding the COVID-19 testing and treatment benefits that can be provided by a high-deductible health plan (HDHP). Under the 2020 guidance, HDHPs can provide those benefits without a deductible or with a deductible below the applicable HDHP minimum deductible (self-only or family), thereby allowing individuals to receive coverage under HDHPs that provide such benefits on a no- or low-deductible basis without any adverse effect on HSA eligibility. Agency FAQs issued earlier this year indicated that the 2020 guidance would apply until further guidance was issued. This latest notice provides that, due to the end of the COVID-19 emergency, the relief described in the 2020 guidance is no longer needed and will apply only for plan years ending on or before December 31, 2024.

The notice also addresses the status of certain items and services as preventive care under the Code’s HSA eligibility rules. According to the notice, the preventive care safe harbor under those rules does not include COVID-19 screening (i.e., testing), effective as of the notice’s publication date. The notice acknowledges that the preventive care safe harbor includes screening services for certain infectious diseases but also observes that screenings for “common and episodic illnesses, such as the flu” are not included and concludes that COVID-19 differs from the types of diseases on the list. The notice further provides that—consistent with recent agency FAQs regarding the impact of the trial court’s decision in the Braidwood case—items and services recommended with an “A” or “B” rating by the United States Preventive Services Task Force (USPSTF) on or after March 23, 2010, are treated as preventive care under the HSA eligibility rules, whether or not they must be covered without cost sharing under the preventive services mandate. Thus, if the USPSTF were to recommend COVID-19 testing with an “A” or “B” rating, then that testing would be treated as preventive care under the HSA eligibility rules, regardless of whether coverage without cost-sharing is required under the preventive services mandate.

QUESTION: Is an opt-out election still available to exempt self-insured state and local governmental plans from compliance obligations under certain group health plan mandates?

ANSWER: Originally, self-insured group health plans of state and local governments could opt out of a wide range of group health plan mandates, including certain HIPAA portability requirements (e.g., special enrollment periods and health status nondiscrimination), the mental health parity rules, standards related to newborns and mothers, reconstructive surgery following mastectomies, and coverage for dependent students on medically necessary leaves of absence (Michelle’s Law). The opt-out right has since been eliminated for certain group health plan mandates, but it is still available for others.

The Affordable Care Act (ACA) eliminated the ability of self-insured plans of state and local governments to opt out of the HIPAA portability requirements for plan years beginning on or after September 23, 2010. And the Consolidated Appropriations Act, 2023 eliminated the election to opt out of compliance with the mental health parity requirements as of December 29, 2022. (No new mental health parity opt-out elections may be made on or after that date, and elections expiring on or after June 27, 2023, may not be renewed. Limited extensions are available for plans subject to multiple collective bargaining agreements.) Still, the opt-out election remains available with respect to three other group health plan mandates: standards related to newborns and mothers, reconstructive surgery following mastectomies, and Michelle’s Law (now obsolete for most plans due to the ACA’s requirement to cover dependent children to age 26). Detailed election and notification requirements apply for plans wishing to rely on the opt-out.

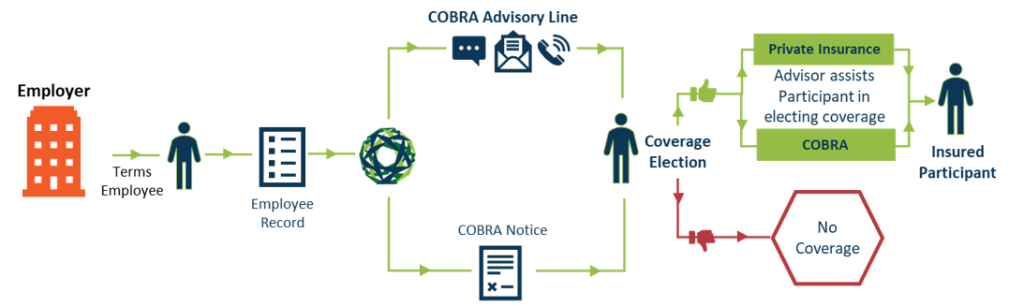

Our new enhanced Cobra solution. COBRAcare+ is a complimentary, cost-saving service offered exclusively by NueSynergy. Participants will get improved engagement through our COBRAcare+ advisory line where they will be guided by a licensed agent to compare COBRA benefits vs. alternative indiviudal health coverage options including subsidies.

QUESTION: We are considering offering a telehealth benefit to our employees that would be separate from our major medical plan. Will this arrangement be an ERISA plan?

ANSWER: Telehealth benefits (also referred to as telemedicine benefits) are often offered under an employer’s group health plan, which is governed by ERISA if sponsored by a private sector employer. Even if telehealth benefits are offered separately from the employer’s group health plan, the benefits are likely subject to ERISA.

In general, an arrangement is an ERISA welfare benefit plan if it is a plan, fund, or program established or maintained by an employer to provide its employees with ERISA-listed benefits. Here is a summary of each element of the definition:

Plan, fund, or program. An arrangement that provides “one-off” benefits and thus does not require an “ongoing administrative scheme” might not be considered a plan, fund, or program subject to ERISA. It is difficult to imagine a telehealth benefit that would not involve ongoing administration, so this element will likely be met.

Established or maintained by an employer for its employees. You have indicated that this benefit would be offered by the company, so this element will be met.

Providing ERISA-listed benefits. Medical benefits are among the benefits listed in ERISA, and telehealth is clearly medical care, so this element will be met.

Under a DOL regulatory safe harbor, certain group insurance arrangements with minimal employer involvement may be exempt from ERISA even if they provide ERISA-listed benefits. If your arrangement is a voluntary employee-pay-all telehealth benefit offered by a third party, with employer involvement limited as set forth in the safe harbor, it would not be an ERISA plan. If it does not meet all the requirements of the safe harbor, it will be an ERISA plan and must comply with the generally applicable rules, such as having a plan administrator, claim and appeal procedures, and a summary plan description.

As a group health plan, a telehealth plan raises legal issues aside from ERISA’s applicability, including considerations under COBRA, HIPAA, and coverage mandates such as first-dollar coverage of preventive services, not imposing annual or lifetime dollar limits on essential health benefits, and parity in mental health and substance use disorder benefits. Note that telehealth-only plans meeting specified criteria have been temporarily exempt from certain of these mandates for certain plan years beginning before the end of the COVID-19 emergency.

Moreover, telehealth coverage may affect an individual’s ability to contribute to a health savings account (HSA), although temporary relief provides that telehealth and other remote care services provided on or after January 1, 2020, will not cause a loss of HSA eligibility for plan years beginning on or before December 31, 2021; for months beginning after March 31, 2022, and before January 1, 2023; and for plan years beginning after December 31, 2022, and before January 1, 2025

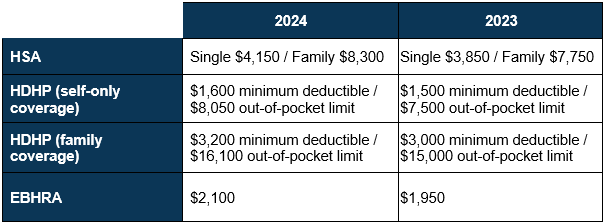

The IRS has just released the 2024 limits for Health Savings Accounts (HSAs) and High Deductible Health Plans (HDHPs). HSA contribution and plan limits will increase to $4,150 for individual coverage and $8,300 for family coverage. Changes to these limits will take effect January 2024.

HSAs are tax-exempt accounts that help people save money for eligible medical expenses. To qualify for an HSA, the policyholder must be enrolled in an HSA-qualified high-deductible health plan, must not be covered by other non-HDHP health insurance or Medicare, and cannot be claimed as a dependent on a tax return.

Question: During the COVID-19 pandemic, we established a telehealth-only plan to provide benefits to individuals who were not eligible for coverage under our regular group health plan. Can we continue to offer this benefit?

ANSWER: During the COVID-19 pandemic, telehealth-only benefits have been exempt from certain requirements that otherwise apply to group health plans. This relief is linked to the COVID-19 public health emergency (PHE), which appears slated to end on May 11, 2023. Once the exemption is no longer available, a telehealth-only plan may continue but it would have to meet those requirements.

As group health plans, telehealth plans must comply with the many rules applicable to group health plans under ERISA, COBRA, HIPAA, and the Affordable Care Act (ACA). The COVID-19 telehealth relief exempts certain plans from the ACA’s prohibition on annual and lifetime limits and its preventive services mandate—but not from other ACA mandates. The relief applies to any arrangement sponsored by a large employer (generally, one with at least 51 employees) that provides solely telehealth and other remote-care benefits and is offered only to employees or dependents who are not eligible for coverage under any other group health plan offered by that employer.

The relief took effect in 2020 and applies for the duration of any plan year beginning before the end of the COVID-19 PHE. If the PHE ends on May 11, 2023, a calendar year telehealth-only plan could remain covered by the exemption until the end of 2023. But if the plan year is, for example, June 1–May 31, the relief applies only until the end of the current plan year on May 31, 2023; as of June 1, 2023, that plan would have to comply with the preventive services mandate and the prohibition on annual and lifetime limits.