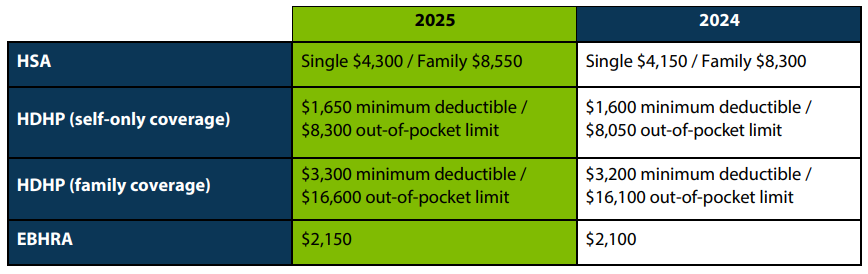

The IRS recently announced the 2025 limits for Health Savings Accounts (HSAs) and High Deductible Health Plans (HDHPs). HSA contribution and plan limits will increase to $4,300 for individual coverage and $8,550 for family coverage. Changes to these limits will take effect January 2025.

HSAs are tax-exempt accounts that help people save money for eligible medical expenses. To qualify for an HSA, the policyholder must be enrolled in an HSA-qualified high-deductible health plan, must not be covered by other non-HDHP health insurance or Medicare, and cannot be claimed as a dependent on a tax return.

In a recent news release, the Internal Revenue Service (IRS) has reiterated important guidelines regarding the eligibility of health and wellness expenses for deductions and reimbursements under health Flexible Spending Arrangements (FSAs), Health Reimbursement Arrangements (HRAs), Health Savings Accounts (HSAs), and Medical Savings Accounts (MSAs).

What Qualifies as a Medical Expense? According to the IRS, for an expense to be considered a medical expense under Code § 213, it must be directly related to the diagnosis, cure, mitigation, treatment, or prevention of disease, or must affect the structure or function of the body. This definition excludes expenses that are solely for general health benefits.

The Risk of Nonmedical Reimbursements: The IRS warns that if health FSAs or other account-based health plans reimburse nonmedical expenses, it could result in all plan payments, including those for legitimate medical expenses, being included in participants’ taxable income.

Misleading Claims and the Importance of Diagnosis-Specific Documentation: The IRS has expressed concerns about companies misleading individuals by suggesting that a doctor’s note can transform general food and wellness expenses into medical expenses. However, without a clear connection to a diagnosis-specific treatment or activity, these expenses do not qualify as medical expenses.

Case in Point: The Denied Claim Highlighting the issue, the IRS shared an instance where an individual with diabetes was denied reimbursement for healthy food expenses through his health FSA. Despite obtaining a doctor’s note from a company that advertised such services, the claim was rejected because the food did not meet the criteria for a medical expense.

Guidance for Taxpayers: For those seeking clarity on what constitutes a reimbursable medical expense, the IRS points to its FAQs on nutrition, wellness, and general health expenses. These resources clarify that food or beverages purchased for health reasons, such as weight loss, can only be reimbursed if they do not fulfill normal nutritional needs, are used to alleviate or treat an illness, and are substantiated by a physician’s prescription.

Understanding the fine line between general wellness and medical care is crucial for taxpayers and plan administrators. As the IRS emphasizes, only expenses that meet the stringent criteria set forth in the Code will be considered for deductions and reimbursements, ensuring the integrity of health-related financial plans.

The IRS announced 2024 contribution limits for all Flexible Spending Account (FSA) plans. Below is an overview of the limit increases across all the types of FSAs except for Dependent Care FSAs, which remain the same at $5,000 per year.

Health Flexible Spending Account

The Health FSA, which provides employees the ability to set aside money on a pre-tax basis to pay for eligible medical, dental, and vision expenses will have an increase to its contribution maximum from $3,050 to $3,200 for 2024. The new contribution limit will also apply to the Limited Purpose FSA which reimburses eligible dental and vision expenses. Limited Purpose FSA limits will also increase from $3,050 to $3,200 for 2024.

Carryover Limit

The FSA Carryover limit provides employers the option to transfer a maximum amount of remaining FSA balances at a plan year’s end to carryover for use during the next plan year. This is available with Healthcare and Limited Purpose FSAs only. The carryover limits for this account will increase from $610 to $640 for 2024.

Commuter Benefits

Commuter Benefits help employees pay for certain parking, mass transit and/or vanpooling expenses with pre-tax dollars. The contribution limits for this account will increase from $300 to $315 for 2024.

Adoption Assistance

The Adoption Assistance FSA helps employees pay eligible adoption expenses such as agency fees and court costs by contributing to the account with pre-tax money from their paycheck. The contribution limits for this account will increase from $15,950 to $16,810 for 2024.

For more information about this major change and how it may impact you, read our latest handout.

The IRS has issued the final versions of Publication 15 (Circular E, Employer’s Tax Guide) and Publication 15-T (Federal Income Tax Withholding Methods) for use in the 2023 tax year.

Publication 15: This publication explains the tax responsibilities as an employer regarding the requirements for withholding, depositing, reporting, paying, and correcting employment taxes. The publication also explains the forms an employer must give to its employees, those employees must provide, and those the employer must send to the IRS and the Social Security Administration (SSA).

Publication 15-T: Publication 15-T supplements Publication 15 and Publication 51 (Agricultural Employer’s Tax Guide). It describes how to figure withholdings using the wage bracket method or percentage method.

Qualified sick/family leave in 2023: Publication 15 notes that the rate of Social Security tax on taxable wages, including qualified sick leave wages and qualified family leave wages paid in 2023 for leave taken between March 31, 2021 – October 1, 2021, is 6.2% each for the employer and employee or 12.4% for both.

However, qualified sick leave wages and qualified family leave wages paid in 2023 for leave taken between March 31, 2020 -April 1, 2021, are not subject to the employer share of Social Security tax; therefore, the tax rate on these wages is 6.2%. The 2023 Social Security wage base limit is $160,200.

Payroll research tax credit: For tax years beginning before January 1, 2023, a qualified small business may elect to claim up to $250,000 of its credit for increasing research activities as a payroll tax credit. The Inflation Reduction Act of 2022 (the IRA) increased the election amount to $500,000 for tax years beginning after December 31, 2022.

The election and determination of the credit amount that will be used against the employer’s payroll taxes are made on Form 6765 (Credit for Increasing Research Activities). The amount from Form 6765, line 44, must then be reported on Form 8974 (Qualified Small Business Payroll Tax Credit for Increasing Research Activities).

Starting in the first quarter of 2023, the payroll tax credit is first used to reduce the employer share of Social Security tax up to $250,000 per quarter and any remaining credit reduces the employer share of Medicare tax for the quarter (any remaining credit is carried forward to the next quarter).

Forms and publications discontinued forms after 2023: Form 941-SS (Employer’s Quarterly Federal Tax Return) and Publications 80 and 179.

During a December 1 payroll industry conference call, the IRS discussed the recent increase in the qualified small business payroll tax credit for increasing research activities as provided under the Inflation Reduction Act.

Background: A provision of the Inflation Reduction Act allows a “qualified small business” (QSB), for tax years beginning after December 31, 2022, to apply an additional $250,000 in qualifying expenses as a payroll tax credit against the employer share of Medicare. Prior to the act, a QSB could apply $250,000 against the employer share of Social Security. The total credit that may be applied will be $500,000 beginning after December 31, 2022. Unused amounts of the credit may be carried over.

Future form revisions: The IRS noted that Form 6765 (Credit for Increasing Research Activities) and its instructions must be revised and will reflect the increased $500,000 limit for the payroll tax credit election. Further, Form 8974 (Qualified Small Business Payroll Tax Credit for Increasing Research Activities) and its instructions must be updated to calculate the amount of credit that can be applied against both Social Security and Medicare. The IRS anticipates the updated forms to be released during the first quarter of 2023.

Claiming the credit: The IRS emphasized that the calculation of the credit does not change on Form 6765 and that only the amount of the credit increases. This form is attached to tax returns as an annual election and cannot be made for the tax year if the election was made for five or more preceding tax years. Taxpayers can claim the credit on Form 941 starting with the first quarter that began after the election. Form 8974 must be completed and attached to Form 941. When the new election with the $500,000 limit is made on Form 6765 that is in effect for 2023 tax year, the IRS expects that it will be claimed in 2024.

Electronic filing of Form 8974: This form is available to be filed electronically. Moreover, Form 8974 can be used to indicate up to a $250,000 credit for the employer share of Social Security and an additional $250,000 credit for the employer share of Medicare. Amounts that are not used can be carried over to a subsequent employment tax return.