QUESTION: We are considering offering a telehealth benefit to our employees that would be separate from our major medical plan. Will this arrangement be an ERISA plan?

ANSWER: Telehealth benefits (also referred to as telemedicine benefits) are often offered under an employer’s group health plan, which is governed by ERISA if sponsored by a private sector employer. Even if telehealth benefits are offered separately from the employer’s group health plan, the benefits are likely subject to ERISA.

In general, an arrangement is an ERISA welfare benefit plan if it is a plan, fund, or program established or maintained by an employer to provide its employees with ERISA-listed benefits. Here is a summary of each element of the definition:

Plan, fund, or program. An arrangement that provides “one-off” benefits and thus does not require an “ongoing administrative scheme” might not be considered a plan, fund, or program subject to ERISA. It is difficult to imagine a telehealth benefit that would not involve ongoing administration, so this element will likely be met.

Established or maintained by an employer for its employees. You have indicated that this benefit would be offered by the company, so this element will be met.

Providing ERISA-listed benefits. Medical benefits are among the benefits listed in ERISA, and telehealth is clearly medical care, so this element will be met.

Under a DOL regulatory safe harbor, certain group insurance arrangements with minimal employer involvement may be exempt from ERISA even if they provide ERISA-listed benefits. If your arrangement is a voluntary employee-pay-all telehealth benefit offered by a third party, with employer involvement limited as set forth in the safe harbor, it would not be an ERISA plan. If it does not meet all the requirements of the safe harbor, it will be an ERISA plan and must comply with the generally applicable rules, such as having a plan administrator, claim and appeal procedures, and a summary plan description.

As a group health plan, a telehealth plan raises legal issues aside from ERISA’s applicability, including considerations under COBRA, HIPAA, and coverage mandates such as first-dollar coverage of preventive services, not imposing annual or lifetime dollar limits on essential health benefits, and parity in mental health and substance use disorder benefits. Note that telehealth-only plans meeting specified criteria have been temporarily exempt from certain of these mandates for certain plan years beginning before the end of the COVID-19 emergency.

Moreover, telehealth coverage may affect an individual’s ability to contribute to a health savings account (HSA), although temporary relief provides that telehealth and other remote care services provided on or after January 1, 2020, will not cause a loss of HSA eligibility for plan years beginning on or before December 31, 2021; for months beginning after March 31, 2022, and before January 1, 2023; and for plan years beginning after December 31, 2022, and before January 1, 2025

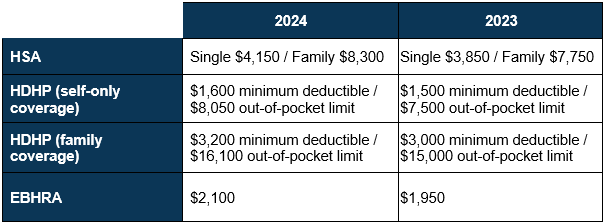

The IRS has just released the 2024 limits for Health Savings Accounts (HSAs) and High Deductible Health Plans (HDHPs). HSA contribution and plan limits will increase to $4,150 for individual coverage and $8,300 for family coverage. Changes to these limits will take effect January 2024.

HSAs are tax-exempt accounts that help people save money for eligible medical expenses. To qualify for an HSA, the policyholder must be enrolled in an HSA-qualified high-deductible health plan, must not be covered by other non-HDHP health insurance or Medicare, and cannot be claimed as a dependent on a tax return.

The IRS has issued FAQs that explain when certain costs related to nutrition, wellness, and general health are medical expenses under Code § 213 that may be paid or reimbursed under a health FSA, HSA, or HRA. As background, Code § 213 defines medical care as amounts paid for the diagnosis, cure, mitigation, treatment, or prevention of disease, or for the purpose of affecting a structure or function of the body. The FAQs explain that medical expenses must be primarily to alleviate or prevent a physical or mental disability or illness, and do not include expenses that are merely beneficial to general health.

The FAQs confirm that the costs of dental, eye, and physical exams are medical expenses that can be paid or reimbursed by a health FSA, HSA, or HRA because these exams diagnose whether a disease or illness is present. The costs of smoking cessation programs and programs that treat drug-related substance use or alcohol use disorders are also medical expenses because they treat a disease. For the cost of therapy to be a medical expense, the therapy must treat a disease—thus, amounts paid for therapy to treat a diagnosed mental illness are medical expenses, while amounts paid for marital counseling are not. Likewise, the costs of nutritional counseling and weight-loss programs are medical expenses only if the counseling or program treats a specific disease diagnosed by a physician (e.g., obesity or diabetes); otherwise, these costs are not medical expenses. The cost of a gym membership is a medical expense only if the membership was purchased for the sole purpose of affecting a structure or function of the body (e.g., a prescribed plan for physical therapy to treat an injury) or treating a specific disease diagnosed by a physician (e.g., obesity or heart disease). However, the cost of exercise for the improvement of general health is not a medical expense, even if recommended by a doctor.

The FAQs also explain the circumstances under which the cost of food or beverages purchased for weight loss or other health reasons will qualify as medical expenses, and that the cost of non-prescription drugs can be paid or reimbursed by a health FSA, HSA, or HRA even though these items (except for insulin) are not deductible under Code § 213. The FAQs confirm that the cost of nutritional supplements is not a medical expense unless the supplements are recommended by a medical practitioner as treatment for a specific medical condition diagnosed by a physician.

QUESTION: Our company sponsors a high-deductible health plan (HDHP) in conjunction with employee HSAs. Can the medical expenses of our employees’ adult children who otherwise qualify for tax-free coverage under the HDHP be reimbursed tax-free from the employees’ HSAs?

ANSWER: Not necessarily—it depends on whether the adult children qualify as tax dependents under the HSA rules. As group health plans, HDHPs that provide dependent coverage of children must make the coverage available until a child turns age 26. (The age 26 mandate does not generally apply to HSAs because they are not group health plans.) The income exclusion for employer-provided health coverage includes employees’ children who are under age 27 as of the end of the taxable year, regardless of whether those children qualify as tax dependents. But similar provisions do not appear in the HSA tax-free reimbursement rules. Instead, whether an adult child’s medical expenses can be reimbursed tax-free from a parent’s HSA depends on whether the child qualifies as a tax dependent for HSA distribution purposes—i.e., whether the adult child is a qualifying child (for example, due to disability) or a qualifying relative (where the parent provides over one-half of the child’s support). Distributions from a parent’s HSA that reimburse a nondependent adult child’s medical expenses are taxable and may be subject to an additional 20% tax.

Thus, the medical expenses of some adult children who are enrolled as dependents in your company’s HDHP will not qualify for tax-free reimbursement from the employee-parent’s HSA. It is possible, however, that these children may be HSA-eligible themselves. If they cannot be claimed as tax dependents and they meet the other HSA eligibility requirements, they could open HSAs of their own.