by admin | May 12, 2026 | Blog

Summer is the perfect time to put your FSA or HSA funds to work. With sunshine, travel, outdoor activities, and heat-driven health concerns, many everyday summer essentials are actually eligible for reimbursement—saving you money while prioritizing your health.

To help you maximize your benefits before funds expire, here are the top five FSA- and HSA-eligible items to purchase this summer, all available through the FSA Store, along with tips on why they matter and how to use them.

1. Sunscreen (SPF 15+)

Why it’s essential:

Excessive sun exposure increases the risk of skin cancer and premature skin aging. Sunscreen is one of the most important summer health investments—and it’s FSA/HSA eligible as long as it provides SPF 15 or higher.

Best uses this summer:

- Beach and pool days

- Outdoor workouts or sports

- Hiking, travel, and everyday commuting

You’ll find mineral, reef-safe, sweat-resistant, and sensitive-skin options available.

👉 Shop FSA/HSA-eligible sunscreen:

https://fsastore.com/fsa-eligible/sunscreen

2. First Aid Kits & Supplies

Why it’s essential:

From scraped knees to blisters and minor burns, summer activities often bring minor injuries. A well-stocked first aid kit keeps you prepared whether you’re camping, traveling, or hosting backyard gatherings.

Eligible items include:

- Adhesive bandages

- Antiseptic wipes

- Burn relief

- Gauze and wound-care products

👉 Browse FSA/HSA-eligible first aid kits:

https://fsastore.com/fsa-eligible/first-aid

3. Allergy Relief Products

Why it’s essential:

Grass pollen, ragweed, and increased outdoor exposure make summer allergies a real challenge. Many over-the-counter allergy treatments are FSA/HSA eligible without a prescription, thanks to IRS rule updates.

Common eligible options:

- Antihistamines

- Nasal sprays

- Eye drops for allergy relief

👉 Shop FSA/HSA-eligible allergy relief:

https://fsastore.com/fsa-eligible/allergy-and-sinus

4. Pain Relief & Recovery Products

Why it’s essential:

Summer activities often mean more movement—and more strain. Whether it’s sore muscles from outdoor workouts, joint discomfort from travel, or minor aches from weekend projects, pain relief and recovery products are among the most practical ways to use FSA or HSA funds.

Common FSA/HSA-eligible options include:

- Over-the-counter pain relievers (acetaminophen, ibuprofen, aspirin)

- Knee, ankle, and wrist braces

- Compression wraps and supports

- Muscle and joint pain relief creams (medicated)

These items are ideal for athletes, travelers, and anyone staying active during warm weather.

👉 Shop FSA/HSA-eligible pain relief & recovery products:

https://fsastore.com/pain-relief-and-recovery/joint-and-muscle-pain

5. Motion Sickness & Travel Health Essentials

Why it’s essential:

Road trips, flights, cruises, and amusement parks peak during summer—and so does motion sickness. Many motion sickness treatments qualify for FSA or HSA reimbursement, helping travelers stay comfortable without extra cost.

Eligible summer favorites include:

- Motion sickness medications

- Wrist bands for nausea relief

- Anti-nausea remedies for travel-related discomfort

These products are especially useful for families, frequent travelers, and those planning long-distance vacations.

👉 Browse FSA/HSA-eligible motion sickness products:

https://fsastore.com/fsa-eligible/motion-sickness

Planning tip: Motion sickness items are often overlooked but can make a major difference in summer travel comfort—making them a smart, proactive FSA/HSA purchase.

Why Buying Summer Essentials With FSA or HSA Funds Makes Sense

Using pre-tax dollars through your Flexible Spending Account (FSA) or Health Savings Account (HSA) can reduce your out-of-pocket healthcare costs by up to 30%, depending on your tax bracket. Summer is an ideal time to stock up because:

- FSAs often have “use-it-or-lose-it” deadlines

- Summer health needs are predictable and recurring

- Many eligible items double as travel and family essentials

The FSA Store only sells products that are verified as FSA/HSA eligible, eliminating reimbursement guesswork.

👉 Start shopping all FSA/HSA-eligible products:

https://fsastore.com

Final Takeaway

If you’re wondering what to buy with your FSA or HSA funds this summer, start with essentials that protect your skin, manage allergies, prevent injuries, and support hydration. These purchases aren’t just eligible—they’re practical, preventative, and seasonally smart.

Stock up now, stay healthy all summer long, and make the most of every pre-tax dollar.

by admin | May 8, 2026 | Blog

Smart HRA, FSA, and HSA Tips to Lower Healthcare Costs

Maximizing your employee health benefits is one of the smartest financial moves you can make each year. Yet many employees enroll in Health Reimbursement Arrangements (HRAs), Flexible Spending Accounts (FSAs), and Health Savings Accounts (HSAs) without fully using the money available to them.

When used strategically, these benefits can significantly reduce out‑of‑pocket healthcare costs, improve cash flow, and even support long‑term financial planning.

This guide shares practical, real‑world tips to maximize your HRA, FSA, and HSA in 2026—so you don’t leave money on the table.

Understanding the Difference Between HRA, FSA, and HSA

Before spending, it’s important to understand how each health benefit account works and what it’s designed to cover.

Health Reimbursement Arrangement (HRA)

An HRA is an employer‑funded account that reimburses employees for eligible medical expenses. Employees do not contribute, and eligible expenses vary by plan.

Flexible Spending Account (FSA)

An FSA allows employees to contribute pre‑tax dollars for qualified healthcare expenses. Many FSAs are subject to a use‑it‑or‑lose‑it rule, making planning essential.

Health Savings Account (HSA)

An HSA is a tax‑advantaged savings account available to employees enrolled in a high‑deductible health plan (HDHP). HSAs offer long‑term savings potential and roll over year after year.

Knowing how these accounts differ is the first step in maximizing your health benefits.

How to Use Your HRA to Reduce Medical Expenses

If your employer offers an HRA, it can dramatically reduce your out‑of‑pocket healthcare costs—especially early in the plan year.

Common HRA‑eligible expenses include:

- Primary care and specialist visits

- Prescription medications

- Diagnostic tests and lab work

- Mental health therapy and counseling

- Physical therapy or chiropractic care

Because HRAs are employer‑funded, using them is like using money your employer has already allocated for your care. Always review your plan’s eligibility guidelines.

Smart Ways to Spend Your FSA Before Funds Expire

A Flexible Spending Account (FSA) helps lower taxable income, but unused funds may be forfeited if not spent by your plan’s deadline.

Popular FSA‑eligible expenses include:

- Vision care (eye exams, glasses, contacts)

- Dental services (cleanings, fillings, orthodontia)

- Over‑the‑counter medications and first‑aid supplies

- Menstrual care products and sunscreen

- Telehealth and virtual mental health services

How to Maximize Your HSA for Short‑ and Long‑Term Savings

A Health Savings Account is often considered one of the most powerful employee benefits due to its triple tax advantage:

- Tax‑deductible contributions

- Tax‑free growth

- Tax‑free withdrawals for qualified medical expenses

Ways to use your HSA effectively:

- Pay deductibles, copays, and prescriptions

- Cover healthcare expenses not fully insured

- Save for future healthcare costs, including retirement medical expenses

Unlike FSAs, HSA funds roll over indefinitely, making them an excellent long‑term healthcare savings strategy.

Combine Your HRA, FSA, and HSA for Maximum Savings

The most effective strategy is often combining benefits:

- Use HRA or FSA funds for immediate healthcare needs

- Preserve HSA funds for future or higher‑cost medical expenses

- Plan spending around rollover rules and tax advantages

Strategic coordination of these accounts can significantly reduce lifetime healthcare costs.

Best Practices for Managing Your Health Benefits

To get the most from your HRA, FSA, and HSA:

- Review eligible expense lists regularly

- Track balances and plan deadlines

- Save receipts and documentation

- Use benefits consistently throughout the year

Staying proactive prevents lost funds and missed opportunities.

Make 2026 the Year You Fully Use Your Health Benefits

Your health benefits are more than open‑enrollment selections—they’re financial tools designed to support your health and budget.

By actively managing your HRA, FSA, and HSA, you can lower healthcare costs, improve financial security, and make smarter decisions year‑round.

Take time to review your benefits today—you may be surprised by how much value you already have access to.

by admin | Apr 17, 2026 | Blog

As Q1 comes to a close, employers are taking a closer look at their benefits to see what’s working, what’s not being used, and how to better support employees. With rising costs and evolving expectations, benefits strategies are shifting toward flexibility, personalization, and real utilization—especially when it comes to FSAs, HSAs, HRAs, and LSAs.

Why Utilization Matters

Unused benefits don’t just represent wasted spend—they reduce the perceived value of a company’s total rewards package. When employees don’t understand how to use their benefits or don’t see how they apply to their lives, engagement suffers.

That’s why employers are using Q1 as a checkpoint to reassess how well their benefits are actually performing.

How Employers Can Analyze Their Benefits

A smarter benefits strategy starts with data. Employers can begin by reviewing:

- Enrollment vs. usage: Are employees signing up for FSAs, HSAs, HRAs, or LSAs—but not spending the funds?

- Average balances and reimbursements: Do accounts sit unused or spike only at year-end?

- Employee demographics and life stages: Are benefits aligned with workforce needs like caregiving, wellness, or long-term savings?

- Employee feedback and questions: What benefits cause confusion or go unused year after year?

This analysis helps identify gaps in education, communication, or relevance—and highlights opportunities to redesign benefits for better outcomes.

The Shift Toward Personalized Benefits

One-size-fits-all benefits no longer meet the needs of today’s workforce. Employers are increasingly offering a mix of accounts so employees can choose what fits them best:

- FSAs for predictable healthcare or dependent care expenses

- HSAs for long-term healthcare and retirement savings

- HRAs to complement health plans with targeted reimbursements

- LSAs for lifestyle, wellness, and everyday flexibility

Personalized benefits lead to higher engagement and stronger employee satisfaction.

The Q1 Takeaway

Benefits that are easy to understand, relevant, and flexible are the ones that get used. And benefits that get used create happier employees and stronger retention.

As employers move into Q2, those who regularly analyze benefits performance—and adjust accordingly—will see the greatest value from their investment.

by admin | Apr 8, 2026 | Blog

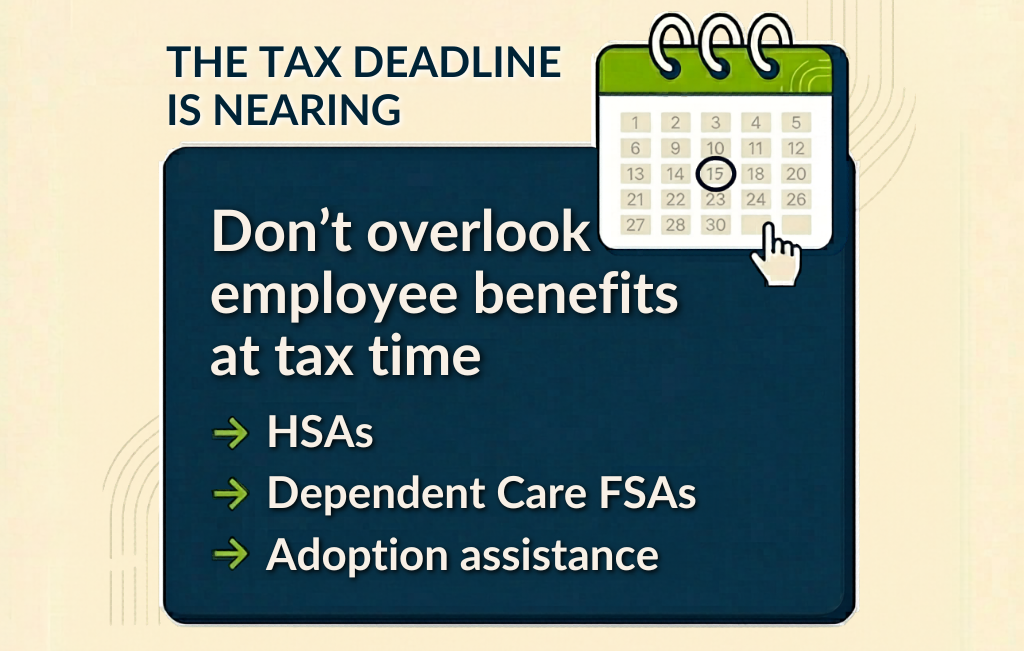

Tax season sneaks up fast, and with the tax deadline right around the corner, it’s easy to forget that some employee benefits come with extra tax forms. If you used certain health or family‑related benefits this year, the IRS may expect a little more information when you file.

The good news? Only a few benefits actually need tax forms. Here’s a quick, simple breakdown.

Used an HSA? You’ll Need to File a Form

If you contributed to a Health Savings Account (HSA) or used HSA money for medical expenses, you’ll need to report it on your tax return.

Forms you may see:

- Form 1099‑SA – Shows how much money you took out of your HSA

- Form 5498‑SA – Shows how much money went into your HSA (for reference)

- Form 8889 – This form must be filed with your tax return

Even if you didn’t spend your HSA money, Form 8889 is still required if you made contributions.

Have a Dependent Care FSA? There’s a Form for That

If you used a Dependent Care FSA to pay for childcare or care for an adult dependent, this benefit must be reported.

Form you’ll need:

- Form 2441 – Dependent Care Expenses

This form helps the IRS make sure your dependent care benefits are reported correctly.

Helpful reminder: Healthcare FSAs do NOT require tax forms—only Dependent Care FSAs do.

Employer Helped With Adoption Costs?

If your employer provided adoption assistance, the IRS requires you to report it.

Form you’ll need:

- Form 8839 – Qualified Adoption Expenses

This form shows how adoption‑related benefits affect your taxes.

Quick Check Before You File

Before you hit “submit,” make sure you have tax forms for:

- HSA contributions or withdrawals

- Dependent Care FSA expenses

- Adoption assistance benefits

Having the right forms ready can help you avoid filing delays, errors, or IRS follow‑ups.

by admin | Jan 12, 2026 | Blog

Flu season is in full swing, and being prepared can make all the difference. The best part? You can use your FSA or HSA funds to stock up on these health essentials without spending extra out-of-pocket.

Here are the top 5 FSA/HSA-approved products to keep you healthy this season:

1. Thermometers

A reliable thermometer is a must for tracking fevers. Digital and smart thermometers are FSA/HSA eligible and help you monitor symptoms accurately.

🔗 Buy a FSA‑eligible thermometer

2. Over-the-Counter Medications

Pain relievers, fever reducers, and cough/cold medicines are often eligible with a prescription. Check your FSA/HSA store for flu symptom relief bundles.

🔗 Shop FSA‑eligible cold & flu meds

3. Humidifiers

Combat dry air and soothe congestion with a humidifier. Many models qualify for FSA/HSA coverage.

🔗 See eligible humidifiers

4. Saline Nasal Sprays

Affordable and effective, saline sprays help relieve nasal congestion and keep your sinuses clear.

🔗 Buy FSA/HSA‑eligible saline spray

5. Face Masks & Hand Sanitizers

Preventing the spread of germs is just as important as treating symptoms. Stock up on masks and sanitizers—both are typically covered.

🔗 Learn about mask & sanitizer eligibility

Why Use FSA/HSA Funds?

Using your tax-free dollars for flu season essentials is a smart way to save money while staying healthy. Don’t forget to check your FSA/HSA store for seasonal deals before your plan year ends!

For a full list of all eligible FSA items click here.