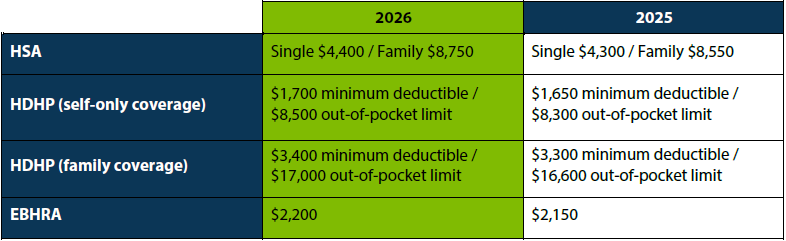

The IRS recently announced the 2026 limits for Health Savings Accounts (HSAs) and High Deductible Health Plans (HDHPs). HSA contribution and plan limits will increase to $4,400 for individual coverage and $8,750 for family coverage. Changes to these limits will take effect January 2026.

HSAs are tax-exempt accounts that help people save money for eligible medical expenses. To qualify for an HSA, the policyholder must be enrolled in an HSA-qualified high-deductible health plan, must not be covered by other non-HDHP health insurance or Medicare, and cannot be claimed as a dependent on a tax return.

In today’s competitive job market, offering attractive employee benefits is crucial for retaining top talent. One effective way to enhance your benefits package is by implementing matching Health Savings Account (HSA) contributions through your company’s cafeteria plan. This blog post will guide you through the process, ensuring compliance with relevant regulations and maximizing the benefits for your employees.

Understanding HSA Contributions and Cafeteria Plans

Health Savings Accounts (HSAs) are tax-advantaged accounts that allow employees to save for medical expenses. Contributions to HSAs can be made by both employees and employers. A cafeteria plan, also known as a Section 125 plan, allows employees to make pre-tax salary reduction contributions to various benefits, including HSAs.

Can Employers Make Matching HSA Contributions?

Yes, employers can make matching contributions to employees’ HSAs through a cafeteria plan. However, it’s essential to understand the regulatory requirements to avoid potential pitfalls.

Comparability Requirements vs. Nondiscrimination Rules

Employers’ HSA contributions are generally subject to comparability requirements, which mandate that contributions must be the same dollar amount or the same percentage of the high-deductible health plan (HDHP) deductible for all eligible employees. This standard effectively prohibits matching contributions, as they would trigger a 35% excise tax on the employer.

However, these comparability requirements do not apply to employer HSA contributions made through a cafeteria plan. Instead, such contributions are subject to the Code § 125 nondiscrimination requirements, which include the eligibility, contributions and benefits, and key employee concentration tests. These tests provide more flexibility for employers to vary HSA contributions on a nondiscriminatory basis.

Designing a Compliant Matching Contribution Plan

To ensure compliance with nondiscrimination rules, carefully design your matching contribution plan. Consider the following:

Eligibility: Ensure that all eligible employees have the opportunity to participate in the HSA matching program.

Contribution Limits: Be mindful of the annual dollar limitations for HSA contributions. All contributions made to an employee’s HSA, whether by the employee, employer, or another entity, must be aggregated for these limits.

Nonforfeitable Contributions: Once made, matching HSA contributions are nonforfeitable. They cannot be subject to a vesting schedule or be returned to the employer if the employee terminates employment midyear.

Communicating the Plan to Employees

Effective communication is key to the success of your HSA matching program. Ensure that the details of the matching contributions are clearly outlined in the cafeteria plan document, summary plan description, and other employee communications, such as open enrollment materials.

Implementing matching HSA contributions through your company’s cafeteria plan can significantly enhance your employee benefits package. By understanding and complying with the relevant regulations, you can offer a valuable benefit that helps attract and retain top talent while providing employees with a tax-advantaged way to save for medical expenses.

For more information on setting up a compliant HSA matching program, reach out to Sales@NueSynergy.com.

Health Savings Accounts (HSAs) are not just for covering medical expenses—they can also be a powerful tool for long-term investment. Recently named as one of the Top HSA providers in 2024 by Morningstar, NueSynergy offers unique investment opportunities that can help you grow your savings while enjoying significant tax benefits. In this blog, we’ll explore how NueSynergy’s HSAs can be leveraged for investment purposes, providing a dual benefit of healthcare savings and wealth accumulation.

Tax Advantages of HSAs

One of the most compelling features of HSAs is their triple tax advantage:

Tax-deductible contributions: Contributions to an HSA are made with pre-tax dollars, reducing your taxable income.

Tax-free growth: Earnings from interest, dividends, and capital gains within the HSA are not taxed.

Tax-free withdrawals: Withdrawals for qualified medical expenses are tax-free.

These benefits make HSAs more advantageous than traditional retirement accounts like 401(k)s and IRAs.

Investing with NueSynergy’s HSAs

NueSynergy stands out for its investment-friendly features. Here are some key points to consider:

1. High-Quality Investment Options

NueSynergy offers an all-ETF lineup, which is the cheapest among its peers, with an average expense ratio of just 0.05%. This low-cost structure allows you to maximize your investment returns. Additionally, as stated in Morningstar, NueSynergy’s investment offerings include no Neutral- or Negative-rated funds, and 64% of its menu was Gold-rated as of August 2024. This high-quality selection ensures that your investments are in reliable and well-performing funds.

2. No Minimum Balance Requirements

NueSynergy does not require a minimum balance to start investing, making it accessible for all account holders. This flexibility allows you to begin investing as soon as you open your HSA, without having to wait until you accumulate a certain balance.

Strategies for Maximizing Investments with NueSynergy

To make the most of your HSA as an investment tool with NueSynergy, consider the following strategies:

1. Maximize Contributions

For 2025, the maximum HSA contribution is $4,300 for individuals and $8,550 for families. If you’re 55 or older, you can contribute an additional $1,000. Maximize your contributions each year to take full advantage of the tax benefits and growth potential.

2. Invest Aggressively Early On

If you’re young and healthy, consider investing aggressively in your HSA. With a longer time horizon, you can afford to take on more risk, which can lead to higher returns.

3. Use Other Funds for Medical Expenses

To allow your HSA investments to grow, try to cover current medical expenses out-of-pocket if possible. This way, your HSA can continue to grow tax-free, providing a larger nest egg for future healthcare costs or retirement.

NueSynergy’s Health Savings Accounts offer a unique opportunity to combine healthcare savings with robust investment potential. By understanding the tax advantages and investment opportunities NueSynergy provides, you can maximize your financial health and secure a more prosperous future.

The HSA Store is akin to the FSA Store, as it’s an outlet for consumers to buy eligible products to fit their Health Savings Account needs. This online store carries over 2,500 products — from first-aid kits, orthodontia to pregnancy tests.

To best utilize the HSA Store, search any HSA eligible item you need for purchase. From there, add a promo code to any purchased HSA eligible item. All promo codes can be turned into points for future purchases.

The smallest denomination of points that can be redeemed for later use is 350 ($10) and largest is 1,500 ($50). You cannot redeem fewer than 350 points at a time. Balances under 350 points cannot be exchanged for a partial value dollar reward. Points expire six months (180 days) following your last order date. To learn about all HSA Store eligible items, look here.

A Health Savings Account (HSA) is an individually owned, tax-favored account that allows participants to pay for qualified healthcare expenses, such as pregnancy test kits, eyeglasses, and more. Here is an overview of the five potential benefits that an HSA provides.

Benefit #1: HSAs provide triple-tax coverage; meaning contributions are made tax-free, grow tax-free, and can be withdrawn tax-free. This is possible if it’s coupled with a High Deductible Health Plan (HDHP).

Benefit #2: Unused HSA funds are rolled over annually, enabling them to be used for future expenses.

Benefit #3: Contribution limits continue to increase with this account. Participants can now use up to $3,850 in annual funds to pay for healthcare expenses individually. If participants wish to use up funds for family coverage, the annual limit is now $7,750.

Benefit #4: Participants who are Medicare eligible, but not enrolled in Medicare, can contribute to an HSA to save for retirement. If 65 or older, HSA funds can also be used without a penalty.

Benefit #5: Even if a participant loses employment, HSA funds can still be used to pay for qualified expenses. However, the ability to continue contributing depends on if the participant chooses to enroll in an HSA qualified health insurance plan either through COBRA, their new employer or an individual policy.