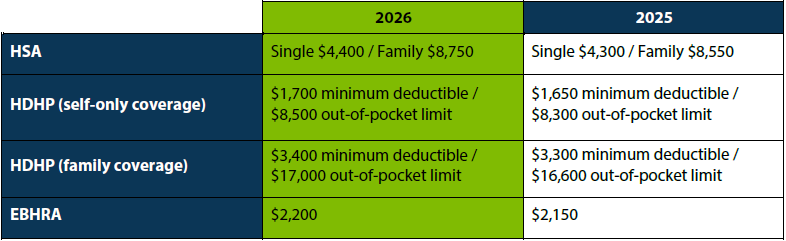

The IRS recently announced the 2026 limits for Health Savings Accounts (HSAs) and High Deductible Health Plans (HDHPs). HSA contribution and plan limits will increase to $4,400 for individual coverage and $8,750 for family coverage. Changes to these limits will take effect January 2026.

HSAs are tax-exempt accounts that help people save money for eligible medical expenses. To qualify for an HSA, the policyholder must be enrolled in an HSA-qualified high-deductible health plan, must not be covered by other non-HDHP health insurance or Medicare, and cannot be claimed as a dependent on a tax return.

The IRS announced the 2025 contribution limits for all Flexible Spending Account (FSA) plans. Below is an overview of the limit increases across all the types of FSAs except for Dependent Care FSAs, which remain the same at $5,000 per year.

Health Flexible Spending Account

The Health FSA, which provides employees the ability to set aside money on a pre-tax basis to pay for eligible medical, dental, and vision expenses will have an increase to its contribution maximum from $3,200 to $3,300 for 2025. The new contribution limit will also apply to the Limited Purpose FSA which reimburses eligible dental and vision expenses. Limited Purpose FSA limits will also increase from $3,200 to $3,300 for 2025.

Carryover Limit

The FSA Carryover limit provides employers the option to transfer a maximum amount of remaining FSA balances at a plan year’s end to carryover for use during the next plan year. This is available with Healthcare and Limited Purpose FSAs only. The carryover limits for this account will increase from $640 to $660 for 2025.

Commuter Benefits

Commuter Benefits help employees pay for certain parking, mass transit, and/or vanpooling expenses with pre-tax dollars. The contribution limits for this account will increase from $315 to $325 for 2025.

Adoption Assistance

The Adoption Assistance FSA helps employees pay eligible adoption expenses such as agency fees and court costs by contributing to the account with pre-tax money from their paycheck. The contribution limits for this account will increase from $16,810 to $17,280 for 2025.

QUESTION: How does the general contribution limit for HSAs work? It is often stated as an annual limit, but isn’t it really monthly? Our company is thinking about changing to HDHP coverage that would allow our employees to make HSA contributions. If we decide to facilitate those HSA contributions or to make employer contributions, would we need to limit the amount of contributions made each month, or only annually?

ANSWER: The general contribution limit for HSAs is an annual limit determined by the number of months of HSA eligibility. The HSA of an individual who is HSA-eligible for the entire year can receive contributions (from any source) up to the full annual limit. If an individual is only HSA-eligible for a portion of the year, the annual limit is prorated based on the number of months of HSA eligibility. A special rule that can change this outcome is noted below.

For example, if Ana, a 40-year-old calendar-year taxpayer, is HSA-eligible for all of 2023 and has self-only HDHP coverage, her HSA can receive contributions of up to the maximum of $3,850 for 2023. (For coverage other than self-only coverage, the maximum for 2023 is $7,750.) If Ana were only HSA-eligible for April through September, however, her annual limit would be 6/12ths of the full annual limit, or $1,925. That $1,925 could be contributed in one month, or in any number of payments made on or after January 1, 2023, and on or before the filing due date (without extensions) for Ana’s 2023 federal tax return. Some or all of the permitted amount could be contributed during a month in which Ana is not HSA-eligible, based on her prior or anticipated months of HSA eligibility. (Of course, contributions could not be made until Ana’s HSA is established, if it wasn’t established by January 1st.) A similar proration rule applies to HSA catch-up contributions, which increase the general contribution limit for HSA-eligible individuals who have attained age 55 by the end of the taxable year. Thus, if Ana were at least age 55 by the end of 2023, and she were HSA-eligible for the entire year, her limit would be increased by $1,000. But if she were HSA-eligible for only 6 months of 2023, her catch-up contribution limit would be only $500.

Employers that facilitate employee contributions or make their own contributions to employees’ HSAs need not limit the amount actually contributed in each month, but they do have to track their employees’ HSA eligibility on a monthly basis so they can determine any prorated limit amount. Employers are only responsible for knowing how their own benefit programs affect HSA eligibility and whether an employee is eligible for catch-up contributions. They need not determine whether employees have disqualifying coverage from other sources or how much has been contributed to employees’ HSAs by other means.

As noted above, special contribution rules can apply when determining a particular employee’s limit. One of these is the “full contribution rule,” which allows calendar-year taxpayers to be treated as HSA-eligible for the entire year if they are HSA-eligible on December 1st, subject to certain conditions that include remaining HSA-eligible for at least a 13-month testing period. There is also a special rule for married individuals if either spouse has family HDHP coverage.

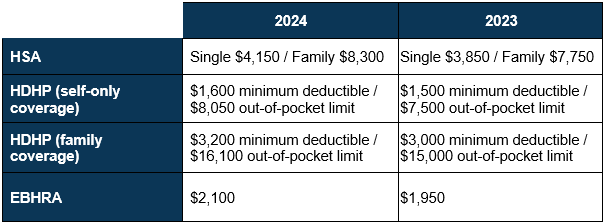

The IRS has just released the 2024 limits for Health Savings Accounts (HSAs) and High Deductible Health Plans (HDHPs). HSA contribution and plan limits will increase to $4,150 for individual coverage and $8,300 for family coverage. Changes to these limits will take effect January 2024.

HSAs are tax-exempt accounts that help people save money for eligible medical expenses. To qualify for an HSA, the policyholder must be enrolled in an HSA-qualified high-deductible health plan, must not be covered by other non-HDHP health insurance or Medicare, and cannot be claimed as a dependent on a tax return.