When managing COBRA coverage, it’s important to know what happens if a qualified beneficiary pays less than the full premium amount. Here’s a simplified guide:

Timely Payments and Grace Periods

Qualified beneficiaries must make timely COBRA premium payments, with a 30-day grace period each month. If the full premium isn’t paid by the end of this period, coverage can be terminated. However, there are special rules for small shortfalls.

What is an Insignificant Shortfall?

An insignificant shortfall is a payment that is less than or equal to the lesser of $50 or 10% of the required premium. For example, if the premium is $490, a shortfall of up to $49 is considered insignificant.

Handling Insignificant Shortfalls

Notify the Beneficiary: Inform them of the shortfall and give them a reasonable period (usually 30 days) to pay the difference.

Grace Period: Allow the beneficiary to pay the remaining amount during this period to avoid termination.

Accept Underpayment: Alternatively, the plan can accept the underpayment as full payment.

Best Practices

Include Procedures: Clearly outline shortfall procedures in your COBRA plan.

Prepare Notices: Have a standard notice ready for shortfalls.

Prompt Notification: Send the notice as soon as a partial payment is received.

By following these steps, you can manage COBRA coverage effectively and ensure compliance with regulations. This helps prevent unnecessary termination and gives beneficiaries a fair chance to maintain their health benefits.

Navigating the intricacies of Dependent Care Assistance Programs (DCAP) can be challenging, especially when it comes to understanding what expenses qualify for reimbursement. One common question that arises is whether application fees, deposits, and similar expenses can be reimbursed. Here, we break down the IRS regulations and provide clarity on this topic.

What Are Indirect Expenses?

Indirect expenses are costs that are not directly for care but are necessary to obtain care. Examples include application fees and deposits paid to day-care centers or preschools. According to IRS regulations, these expenses may qualify for reimbursement under a DCAP if they meet specific criteria.

Criteria for Reimbursement

To be eligible for reimbursement, indirect expenses must:

Be Required for Care: The employee must be required to pay these expenses to obtain related care.

Meet DCAP Rules: The expenses must comply with DCAP rules and the plan document.

Relate to Provided Care: The care to which these expenses relate must actually be provided.

Examples of Reimbursable and Non-Reimbursable Expenses

Reimbursable: If a DCAP participant pays a $100 application fee to secure a spot at a new day-care provider, this fee can be reimbursed once the care is provided.

Non-Reimbursable: If a participant pays a $100 deposit to a preschool but later decides not to enroll the child, the deposit is not reimbursable since the care was not provided.

Timing of Reimbursement

The IRS does not specify whether indirect expenses can be reimbursed in full once care commences or if they must be reimbursed proportionately over the duration of the care agreement. To err on the side of caution, it is advisable to prorate the reimbursement over the agreement’s duration. For instance, if the agreement is month-to-month, the entire fee might be reimbursed after the first month of care. For longer agreements, the fee should be prorated accordingly.

Conclusion

Understanding the nuances of DCAP reimbursements for indirect expenses like application fees and deposits is crucial for both employers and employees. By ensuring these expenses meet the necessary criteria and timing the reimbursements appropriately, you can navigate the DCAP rules effectively and make the most of your benefits.

In today’s competitive job market, offering attractive employee benefits is crucial for retaining top talent. One effective way to enhance your benefits package is by implementing matching Health Savings Account (HSA) contributions through your company’s cafeteria plan. This blog post will guide you through the process, ensuring compliance with relevant regulations and maximizing the benefits for your employees.

Understanding HSA Contributions and Cafeteria Plans

Health Savings Accounts (HSAs) are tax-advantaged accounts that allow employees to save for medical expenses. Contributions to HSAs can be made by both employees and employers. A cafeteria plan, also known as a Section 125 plan, allows employees to make pre-tax salary reduction contributions to various benefits, including HSAs.

Can Employers Make Matching HSA Contributions?

Yes, employers can make matching contributions to employees’ HSAs through a cafeteria plan. However, it’s essential to understand the regulatory requirements to avoid potential pitfalls.

Comparability Requirements vs. Nondiscrimination Rules

Employers’ HSA contributions are generally subject to comparability requirements, which mandate that contributions must be the same dollar amount or the same percentage of the high-deductible health plan (HDHP) deductible for all eligible employees. This standard effectively prohibits matching contributions, as they would trigger a 35% excise tax on the employer.

However, these comparability requirements do not apply to employer HSA contributions made through a cafeteria plan. Instead, such contributions are subject to the Code § 125 nondiscrimination requirements, which include the eligibility, contributions and benefits, and key employee concentration tests. These tests provide more flexibility for employers to vary HSA contributions on a nondiscriminatory basis.

Designing a Compliant Matching Contribution Plan

To ensure compliance with nondiscrimination rules, carefully design your matching contribution plan. Consider the following:

Eligibility: Ensure that all eligible employees have the opportunity to participate in the HSA matching program.

Contribution Limits: Be mindful of the annual dollar limitations for HSA contributions. All contributions made to an employee’s HSA, whether by the employee, employer, or another entity, must be aggregated for these limits.

Nonforfeitable Contributions: Once made, matching HSA contributions are nonforfeitable. They cannot be subject to a vesting schedule or be returned to the employer if the employee terminates employment midyear.

Communicating the Plan to Employees

Effective communication is key to the success of your HSA matching program. Ensure that the details of the matching contributions are clearly outlined in the cafeteria plan document, summary plan description, and other employee communications, such as open enrollment materials.

Implementing matching HSA contributions through your company’s cafeteria plan can significantly enhance your employee benefits package. By understanding and complying with the relevant regulations, you can offer a valuable benefit that helps attract and retain top talent while providing employees with a tax-advantaged way to save for medical expenses.

For more information on setting up a compliant HSA matching program, reach out to Sales@NueSynergy.com.

The IRS has released the optional standard mileage rates for 2025, providing important updates for businesses, medical care, and charitable activities. Here’s what you need to know about the new rates and vehicle value limits.

2025 Standard Mileage Rates

Business Use: The standard mileage rate for business use of an automobile has increased to 70 cents per mile, up from 67 cents in 2024. This rate can be used instead of calculating actual expenses like depreciation, lease payments, and fuel costs.

Medical and Moving Use: The rate for using an automobile to obtain medical care or for moving expenses remains unchanged at 21 cents per mile. This rate applies to variable expenses only, such as gas and oil, and does not include fixed costs like depreciation and insurance.

Charitable Use: The rate for charitable use of an automobile remains at 14 cents per mile.

Understanding the Rates

The standard mileage rates offer a simplified method for taxpayers to deduct automobile expenses. For business use, the rate covers both fixed and variable costs, while for medical and moving purposes, only variable costs are deductible. Parking fees and tolls related to medical or moving expenses can be deducted separately.

Vehicle Value Limits

The IRS has also set the maximum vehicle values for 2025, which determine the applicability of certain valuation rules for employer-provided vehicles:

Cents-Per-Mile Rule: This rule values personal use of an employer-provided vehicle by multiplying the business standard mileage rate by the number of personal miles driven.

Fleet-Average Valuation Rule: Employers with a fleet of 20 or more vehicles can use an average annual lease value for each vehicle in the fleet.

For vehicles first made available for personal use in 2025, the maximum vehicle value under both rules is $61,200, down from $62,000 in 2024. This value also sets the maximum standard automobile cost for reimbursement allowances under a fixed and variable rate (FAVR) plan.

These updates from the IRS provide clarity and consistency for taxpayers planning their 2025 automobile expenses. By understanding and utilizing the new standard mileage rates and vehicle value limits, individuals and businesses can better manage their tax deductions and compliance.

Employee benefits often include a lot of acronyms. What do these and other acronyms mean? They are primarily used in Cafeteria Plans, Consumer-Driven Health Care, ERISA Compliance, COBRA, HIPAA, and Group Health Plan Mandates manuals. The list below provides a comprehensive collection of all the acronyms used.

AD&D Plan – Accidental Death and Dismemberment Plan

ADA – Americans with Disabilities Act

ASG – Affiliated Service Group

ASO – Administrative-Services-Only

ATIN – Adoption Taxpayer Identification Number

CE – Covered Entity

CMS – Center for Medicare and Medicaid Services

COB – Coordination of Benefits

COBRA – Consolidated Omnibus Budget Reconciliation Act

COLA – Cost-of-Living Adjustment

CONUS – Continental United States

DCAP – Dependent Care Assistance Program

DCTC – Dependent Care Tax Credit

DFVC Program – Delinquent Filer Voluntary Compliance Program

DOL – Department of Labor

EAP – Employee Assistance Plan

EBHRA – Excepted Benefit HRA

EBSA – Employee Benefits Security Administration

EDI – Electronic Data Interchange

EFAST2 – ERISA Filing Acceptance System II (electronic submission of Form 5500s)

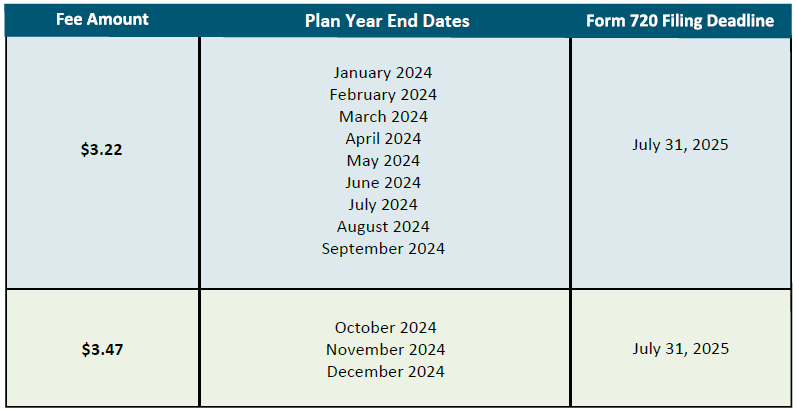

The IRS has released the 2025 Patient-Centered Outcomes Research (PCORI) fee amounts for health insurers and self-insured health plan sponsors. The PCORI fee is due on July 31, 2025. For plan and policy years ending between October 1, 2024, and October 1, 2025, the PCORI fee is $3.47 per covered life, up from $3.22 for the previous year. This is a $.25 increase from the amount in effect for plan and policy years ending on or after October 1, 2023, and before October 1, 2024.

PCORI fees are calculated by multiplying the applicable dollar amount for the year by the plans or policy’s average number of covered lives. These fees, established by the Affordable Care Act (ACA), fund clinical effectiveness research.

Below is the fee amount per plan year.

For more information on the upcoming PCORI fee deadline please refer to the IRS’ PCORI fee FAQ