As employers prepare to offer health flexible spending accounts (FSAs), a common question arises: Are health FSAs administered by third-party administrators (TPAs) subject to HIPAA’s privacy and security rules? The short answer is yes—and here’s why that matters.

Understanding HIPAA’s Scope for Health FSAs

Under HIPAA, a health FSA is considered a group health plan, which makes it a covered entity subject to HIPAA’s privacy and security rules. The only exception is for self-administered FSAs with fewer than 50 participants—a rare scenario for most employers.

If your company uses a TPA to manage FSA claims, this exception does not apply. That means your health FSA must comply with HIPAA’s full privacy and security requirements.

Why Fully Insured Plans Are Different

Employers with fully insured major medical plans often take a “hands-off” approach to protected health information (PHI), receiving only summary or enrollment data. This limits their HIPAA obligations because the insurer, not the employer, handles PHI.

However, most health FSAs are self-insured, and the “hands-off” exception doesn’t apply. Even if a TPA handles the day-to-day administration, your company is still responsible for HIPAA compliance.

What Employers Must Do

To comply with HIPAA when offering a TPA-administered health FSA, employers should:

Enter into a Business Associate Agreement (BAA) with the TPA, outlining how PHI will be handled.

Implement privacy and security policies for the health FSA.

Limit internal access to PHI to only those who need it for plan administration.

Train staff who may come into contact with PHI.

Ensure electronic PHI (ePHI) is protected under HIPAA’s security rule.

Minimizing Risk and Burden

While you can’t avoid HIPAA obligations entirely, you can minimize your exposure by delegating as much as possible to the TPA. This reduces the amount of PHI your company accesses and simplifies compliance.

If your company is offering a health FSA administered by a TPA, you are subject to HIPAA’s privacy and security rules. Taking proactive steps to comply—especially by working closely with your TPA—will help protect employee data and reduce legal risk.

If your business hires extra help during the holidays, you might wonder if you’re required to offer health insurance. That depends on whether you’re an Applicable Large Employer (ALE) under the Affordable Care Act (ACA).

What’s an ALE?

You’re an ALE if you had 50 or more full-time employees (or equivalents) on average last year. If you are, you must offer affordable health insurance to at least 95% of your full-time employees and their children—or you could face penalties.

How to Count Employees

Count full-time employees (30+ hours/week).

Add part-time hours together and divide by 120 to get full-time equivalents (FTEs).

Average the total number of full-time + FTEs for each month of the year.

Seasonal Worker Exception

You’re not an ALE if:

You go over 50 employees for 120 days or fewer, and

The extra workers are seasonal (like holiday retail staff).

So, if you usually have 40 employees and hire 80 more just for November and December, you likely don’t have to offer health insurance—as long as those extra workers are seasonal.

Quick Tip

“Seasonal worker” helps decide if you’re an ALE. “Seasonal employee” matters only if you’re already an ALE and need to track who’s full-time.

Bottom line: If your workforce only grows during the holidays, you may not be required to offer health benefits. But if you’re an ALE, you must offer coverage—or face penalties.

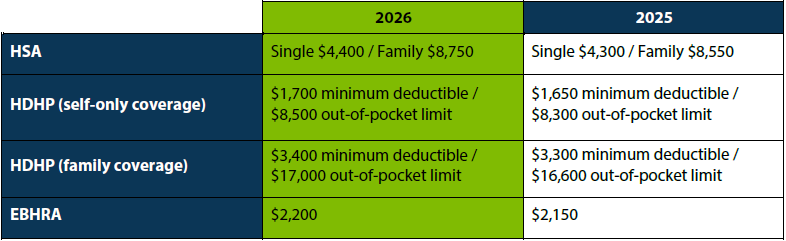

The IRS recently announced the 2026 limits for Health Savings Accounts (HSAs) and High Deductible Health Plans (HDHPs). HSA contribution and plan limits will increase to $4,400 for individual coverage and $8,750 for family coverage. Changes to these limits will take effect January 2026.

HSAs are tax-exempt accounts that help people save money for eligible medical expenses. To qualify for an HSA, the policyholder must be enrolled in an HSA-qualified high-deductible health plan, must not be covered by other non-HDHP health insurance or Medicare, and cannot be claimed as a dependent on a tax return.

Navigating cafeteria plans can be tricky for both employers and employees. A common question is whether financial hardship allows midyear election changes to health FSAs. Unfortunately, it doesn’t.

Why Financial Hardship Isn’t a Qualifying Event

IRS rules state that cafeteria plan elections are irrevocable for the plan year unless a qualifying event occurs. Financial hardship, such as buying a new house and facing unexpected expenses, does not qualify as a permitted election change event.

Qualifying Events for Election Changes

The IRS outlines specific events that allow for midyear election changes, including:

Change in marital status

Change in the number of dependents

Change in employment status

Significant cost or coverage changes (not applicable to health FSAs)

Qualified medical child support orders

Since financial hardship does not fall under these categories, employees must wait until the next open enrollment period to make changes to their health FSA elections.

Communicating Plan Rules

To minimize confusion and potential employee relations issues, employers should clearly communicate the rules and limitations of their cafeteria plans. Providing real-life examples can help employees understand which events qualify for election changes and which do not. This proactive approach can prevent misunderstandings and ensure employees are well-informed.

Plan Design Considerations

Employers may also consider redesigning their health FSA plans to eliminate midyear election changes altogether, except in cases of qualified medical child support orders. This can simplify plan administration and reduce the challenges associated with determining coverage amounts for the remainder of the plan year.

While financial hardship is a difficult situation for any employee, it does not justify a midyear election change to a health FSA under current IRS rules. Employers can support their employees by providing clear communication about plan rules and considering plan design adjustments to streamline administration. By taking these steps, employers can help ensure a smooth and compliant operation of their cafeteria plans.

Navigating the complexities of the Family and Medical Leave Act (FMLA) can be challenging, especially when it comes to maintaining health coverage for employees on unpaid leave. This guide will help you understand what to do when an employee on FMLA leave fails to pay their health insurance premiums on time, and how it affects Flexible Spending Accounts (FSAs), Health Reimbursement Arrangements (HRAs), Health Savings Accounts (HSAs), and COBRA.

Employer Obligations

Under FMLA, employers must maintain health coverage for employees on leave as if they were still working. This obligation ends if the premium payment is over 30 days late, unless your company policy allows a longer grace period.

Steps Before Dropping Coverage

Before dropping an employee’s health coverage, provide written notice at least 15 days before coverage ends, specifying the termination date if payment isn’t received. Send the notice at least 15 days before the end of the grace period.

Termination of Coverage

Coverage can be terminated retroactively if your company policy allows, otherwise, it ends prospectively at the grace period’s end.

Impact on FSAs, HRAs, and HSAs

FSAs: Employees can choose to continue or revoke their FSA coverage during unpaid FMLA leave. Payment options include pre-pay, pay-as-you-go, and catch-up contributions.

HRAs: Employers must extend COBRA rights to HRAs. Employees can use their HRA balance during COBRA coverage, and employers should calculate a reasonable premium for the HRA.

HSAs: Employees can continue contributing to their HSA during COBRA coverage and use HSA funds to pay for COBRA premiums.

COBRA and ACA Rules

A COBRA election notice isn’t required for coverage loss due to nonpayment. However, failure to return to work after FMLA leave is a COBRA qualifying event. ACA allows cancellation for nonpayment, but stricter state laws may apply.

Restoring Coverage

If an employee returns from FMLA leave after coverage was dropped, their health coverage must be restored.

Managing health coverage for employees on FMLA leave requires careful attention to legal requirements and company policies. By following these steps, you can ensure compliance and support your employees during their leave.

HIPAA special enrollment rights allow eligible employees to enroll in health plans outside the regular enrollment period due to specific life events. These rights also impact Health Reimbursement Arrangements (HRAs), Health Savings Accounts (HSAs), and Flexible Spending Accounts (FSAs).

When and Who Receives the Notice?

Notices must be provided to all eligible employees at or before the time they are first offered the opportunity to enroll. This includes employees who:

Decline coverage due to other health insurance and later lose eligibility.

Become eligible for state premium assistance under Medicaid or CHIP.

Acquire a new spouse or dependent by marriage, birth, adoption, or placement for adoption.

What Should the Notice Include?

The notice must describe special midyear enrollment opportunities and inform participants about deadlines for enrollment requests—30 days for most events, 60 days for Medicaid or CHIP-related events.

Distribution Methods

Include the notice with plan enrollment materials and, if conditions are met, distribute it electronically.

Impact on HRAs, HSAs, and FSAs

Special enrollment rights can affect contributions and usage of HRAs, HSAs, and FSAs:

HRAs: Adjust contributions or usage to align with new coverage.

HSAs: Review HSA contributions and ensure compliance with IRS rules.

FSAs: Update FSA elections to reflect changes in coverage or dependent status.

Consequences of Non-Compliance

Failing to provide the notice timely can lead to enrollment issues and potential penalties from the Department of Labor (DOL).

Providing HIPAA special enrollment notices is essential for compliance and helps employees make informed decisions about their health coverage and financial accounts. Understanding the impact on HRAs, HSAs, and FSAs ensures that employees can effectively manage their health-related financial accounts in conjunction with their health plan enrollment.