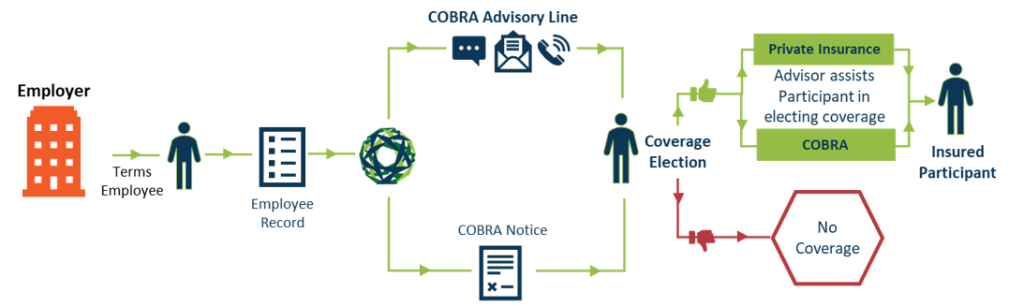

Our new enhanced Cobra solution. COBRAcare+ is a complimentary, cost-saving service offered exclusively by NueSynergy. Participants will get improved engagement through our COBRAcare+ advisory line where they will be guided by a licensed agent to compare COBRA benefits vs. alternative indiviudal health coverage options including subsidies.

QUESTION: Due to the COVID-19 emergency, we have been required to extend deadlines for participants and beneficiaries to submit claims and appeals under our employee benefit plans. How does the end of the COVID-19 national emergency affect these extensions?

ANSWER: As you note, various plan-related deadlines have been extended—but for no longer than one year—by disregarding (tolling) the COVID-19 “outbreak period,” which ends 60 days after the end of the national emergency unless another end date is announced by the agencies. The COVID-19 national emergency ended on April 10, 2023. Although 60 days later would be June 9, 2023, the DOL has informally commented that, consistent with FAQs issued in March 2023, the outbreak period will end on July 10, 2023.

The outbreak period relief extends the deadlines for individuals to file claims for benefits and appeals of adverse benefit determinations under employee benefit plans that are subject to ERISA or the Code—including group health plans, disability and other employee welfare benefit plans, and retirement plans. For group health plans, the extension also applies to deadlines for requesting external review following exhaustion of the plan’s internal appeals procedures and for perfecting an incomplete request for review. The disregarded period lasts until the earlier of (1) one year from the date the individual was first eligible for outbreak period relief, or (2) the end of the outbreak period. Once the disregarded period has ended, the regular timeframes resume. Thus, the extended deadline must be determined on an individual basis. For example:

Alex, a participant in a group health plan that normally requires claims to be submitted within one year after the date of service, received medical care on July 1, 2022. The disregarded period begins on the service date (July 1, 2022) and ends on the earlier of one year later (July 1, 2023) or the end of the outbreak period (July 10, 2023). Thus, the plan’s regular one-year timeline begins to run on July 1, 2023, so the deadline for Alex to submit a claim is July 1, 2024. For medical care received on August 1, 2022, the disregarded period would end on July 10, 2023 (the earlier of the end of the outbreak period or one year after the service date), and then the plan’s regular one-year timeline would begin to run, so the deadline for submitting a claim would be July 10, 2024.

Note that a different interpretation of the extension—applying the plan’s timeline first and the outbreak period relief after the end of the regular timeline—would produce a different result in some circumstances. Applying this interpretation to the first example above, the claim submission deadline would be July 10, 2023 (the earlier of July 10, 2023, or one year after the July 1, 2023, regular claim submission deadline). Given that the agencies, in the FAQs, encouraged plans to allow participants and beneficiaries more time to act, it seems advisable to take the approach that results in the later deadline. In any event, clear communication and consistency in application will be important.

Although plans were not expressly granted more time to process and decide claims, the DOL recognized that the COVID-19 emergency may present challenges in achieving “full and timely compliance” with ERISA’s claims procedure requirements and said that its approach to enforcement would emphasize compliance assistance. But at this late stage of the pandemic, it seems unlikely that the DOL would grant plans much leeway in this regard.