When managing group health insurance plans, employers often face the challenge of aligning COBRA premiums with midyear increases in insurance premiums. However, the IRS COBRA regulations generally do not permit midyear increases in COBRA premiums. Here’s what you need to know:

Understanding COBRA Premiums

COBRA (Consolidated Omnibus Budget Reconciliation Act) allows qualified beneficiaries to continue their group health coverage after certain qualifying events, such as job loss. The premium for COBRA coverage is capped at 102% of the “applicable premium” for the coverage, which can increase to 150% during a disability extension.

Fixed Determination Period

The applicable premium must be computed and fixed before the start of a 12-month “determination period” and generally cannot be changed until the next determination period. This means that even if your insurer increases premiums midyear, you cannot pass this increase onto COBRA beneficiaries until the next determination period.

Exceptions to the Rule

There are three exceptions to this general rule:

Disability Extension: If a qualified beneficiary’s maximum coverage period is extended due to disability, the premium can increase from 102% to 150%.

Undercharging: If the plan is charging less than the maximum permissible amount (102%), it can increase the COBRA premium to that level.

Coverage Changes: If a qualified beneficiary changes coverage from one benefit package or coverage unit to another, the premium can be adjusted to the new rate determined before the determination period began.

Strategic Planning for Employers

To avoid the complications of midyear premium increases, employers should:

Align the insurer’s rate period with the plan’s 12-month COBRA determination period.

Lock in the premium charged by the insurer for the entire determination period, at least for COBRA purposes.

By understanding and planning for these regulations, employers can better manage their COBRA premiums and ensure compliance with IRS rules.

Administering a Health Flexible Spending Account (FSA) can be challenging, especially when employees request midyear changes to their elections due to unforeseen medical circumstances. This blog post aims to clarify the rules surrounding midyear election changes and provide practical tips for employers to manage these situations effectively.

Can Employees Change Health FSA Elections Midyear?

Question: Can employees reduce their Health FSA contributions if they are prevented from receiving anticipated medical care after enrollment?

Answer: No, employees cannot change their Health FSA elections under these circumstances. According to IRS regulations, an employee’s Health FSA election is irrevocable during a plan year unless an event occurs that fits within one of the exceptions available under IRS regulations or other guidance. Changes in medical condition or a provider’s recommendation do not qualify as changes in status and do not fall within the other exceptions applicable to Health FSAs.

Examples of Non-Qualifying Situations

Pregnancy and Laser Eye Surgery: If a doctor refuses to perform laser eye surgery on an employee who is pregnant, the employee cannot change their Health FSA election.

Dental Work Changes: If an employee’s spouse does not undergo planned dental work because the dentist’s recommendation changed, the employee cannot adjust their Health FSA contributions.

These situations do not qualify as “mistakes” that would allow an election change. The IRS’s 2007 proposed cafeteria plan regulations include an example where an employee elects Health FSA salary reductions for the next plan year in anticipation of eye surgery. If the surgery cannot be performed after the plan year starts, the employee must forfeit the remaining balance under the use-or-lose rule if their other eligible medical expenses are less than the amount contributed.

Minimizing Employee Relations Issues

While election changes are not allowed under these circumstances, employers can take steps to minimize employee relations issues:

Clear Communication: Ensure that enrollment and other materials clearly explain the limited reasons for midyear election changes. Including real-life examples can be helpful.

Remind Employees of Eligible Expenses: Employees may still use the funds by submitting other eligible expenses for reimbursement.

Plan Amendments: Consider amending your plan to allow Health FSA carryovers of up to $660 to the next plan year. The maximum carryover amount is indexed, so stay updated on the latest limits.

Grace Period: Adopt a grace period to give employees extra time to use up remaining funds.

By proactively addressing these issues, employers can help employees better understand their Health FSA options and reduce frustration related to midyear election changes.

Navigating the intricacies of Dependent Care Assistance Programs (DCAP) can be challenging, especially when it comes to understanding what expenses qualify for reimbursement. One common question that arises is whether application fees, deposits, and similar expenses can be reimbursed. Here, we break down the IRS regulations and provide clarity on this topic.

What Are Indirect Expenses?

Indirect expenses are costs that are not directly for care but are necessary to obtain care. Examples include application fees and deposits paid to day-care centers or preschools. According to IRS regulations, these expenses may qualify for reimbursement under a DCAP if they meet specific criteria.

Criteria for Reimbursement

To be eligible for reimbursement, indirect expenses must:

Be Required for Care: The employee must be required to pay these expenses to obtain related care.

Meet DCAP Rules: The expenses must comply with DCAP rules and the plan document.

Relate to Provided Care: The care to which these expenses relate must actually be provided.

Examples of Reimbursable and Non-Reimbursable Expenses

Reimbursable: If a DCAP participant pays a $100 application fee to secure a spot at a new day-care provider, this fee can be reimbursed once the care is provided.

Non-Reimbursable: If a participant pays a $100 deposit to a preschool but later decides not to enroll the child, the deposit is not reimbursable since the care was not provided.

Timing of Reimbursement

The IRS does not specify whether indirect expenses can be reimbursed in full once care commences or if they must be reimbursed proportionately over the duration of the care agreement. To err on the side of caution, it is advisable to prorate the reimbursement over the agreement’s duration. For instance, if the agreement is month-to-month, the entire fee might be reimbursed after the first month of care. For longer agreements, the fee should be prorated accordingly.

Conclusion

Understanding the nuances of DCAP reimbursements for indirect expenses like application fees and deposits is crucial for both employers and employees. By ensuring these expenses meet the necessary criteria and timing the reimbursements appropriately, you can navigate the DCAP rules effectively and make the most of your benefits.

The IRS has released the optional standard mileage rates for 2025, providing important updates for businesses, medical care, and charitable activities. Here’s what you need to know about the new rates and vehicle value limits.

2025 Standard Mileage Rates

Business Use: The standard mileage rate for business use of an automobile has increased to 70 cents per mile, up from 67 cents in 2024. This rate can be used instead of calculating actual expenses like depreciation, lease payments, and fuel costs.

Medical and Moving Use: The rate for using an automobile to obtain medical care or for moving expenses remains unchanged at 21 cents per mile. This rate applies to variable expenses only, such as gas and oil, and does not include fixed costs like depreciation and insurance.

Charitable Use: The rate for charitable use of an automobile remains at 14 cents per mile.

Understanding the Rates

The standard mileage rates offer a simplified method for taxpayers to deduct automobile expenses. For business use, the rate covers both fixed and variable costs, while for medical and moving purposes, only variable costs are deductible. Parking fees and tolls related to medical or moving expenses can be deducted separately.

Vehicle Value Limits

The IRS has also set the maximum vehicle values for 2025, which determine the applicability of certain valuation rules for employer-provided vehicles:

Cents-Per-Mile Rule: This rule values personal use of an employer-provided vehicle by multiplying the business standard mileage rate by the number of personal miles driven.

Fleet-Average Valuation Rule: Employers with a fleet of 20 or more vehicles can use an average annual lease value for each vehicle in the fleet.

For vehicles first made available for personal use in 2025, the maximum vehicle value under both rules is $61,200, down from $62,000 in 2024. This value also sets the maximum standard automobile cost for reimbursement allowances under a fixed and variable rate (FAVR) plan.

These updates from the IRS provide clarity and consistency for taxpayers planning their 2025 automobile expenses. By understanding and utilizing the new standard mileage rates and vehicle value limits, individuals and businesses can better manage their tax deductions and compliance.

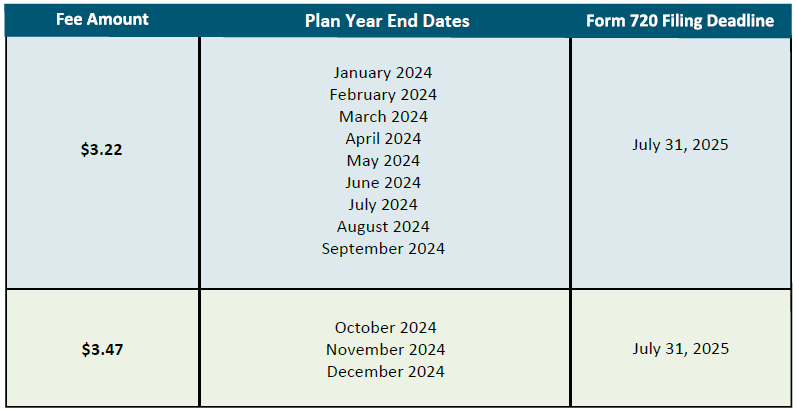

The IRS has released the 2025 Patient-Centered Outcomes Research (PCORI) fee amounts for health insurers and self-insured health plan sponsors. The PCORI fee is due on July 31, 2025. For plan and policy years ending between October 1, 2024, and October 1, 2025, the PCORI fee is $3.47 per covered life, up from $3.22 for the previous year. This is a $.25 increase from the amount in effect for plan and policy years ending on or after October 1, 2023, and before October 1, 2024.

PCORI fees are calculated by multiplying the applicable dollar amount for the year by the plans or policy’s average number of covered lives. These fees, established by the Affordable Care Act (ACA), fund clinical effectiveness research.

Below is the fee amount per plan year.

For more information on the upcoming PCORI fee deadline please refer to the IRS’ PCORI fee FAQ