As employers prepare to offer health flexible spending accounts (FSAs), a common question arises: Are health FSAs administered by third-party administrators (TPAs) subject to HIPAA’s privacy and security rules? The short answer is yes—and here’s why that matters.

Understanding HIPAA’s Scope for Health FSAs

Under HIPAA, a health FSA is considered a group health plan, which makes it a covered entity subject to HIPAA’s privacy and security rules. The only exception is for self-administered FSAs with fewer than 50 participants—a rare scenario for most employers.

If your company uses a TPA to manage FSA claims, this exception does not apply. That means your health FSA must comply with HIPAA’s full privacy and security requirements.

Why Fully Insured Plans Are Different

Employers with fully insured major medical plans often take a “hands-off” approach to protected health information (PHI), receiving only summary or enrollment data. This limits their HIPAA obligations because the insurer, not the employer, handles PHI.

However, most health FSAs are self-insured, and the “hands-off” exception doesn’t apply. Even if a TPA handles the day-to-day administration, your company is still responsible for HIPAA compliance.

What Employers Must Do

To comply with HIPAA when offering a TPA-administered health FSA, employers should:

Enter into a Business Associate Agreement (BAA) with the TPA, outlining how PHI will be handled.

Implement privacy and security policies for the health FSA.

Limit internal access to PHI to only those who need it for plan administration.

Train staff who may come into contact with PHI.

Ensure electronic PHI (ePHI) is protected under HIPAA’s security rule.

Minimizing Risk and Burden

While you can’t avoid HIPAA obligations entirely, you can minimize your exposure by delegating as much as possible to the TPA. This reduces the amount of PHI your company accesses and simplifies compliance.

If your company is offering a health FSA administered by a TPA, you are subject to HIPAA’s privacy and security rules. Taking proactive steps to comply—especially by working closely with your TPA—will help protect employee data and reduce legal risk.

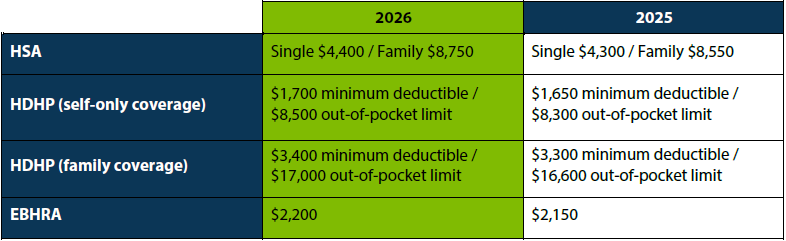

The IRS recently announced the 2026 limits for Health Savings Accounts (HSAs) and High Deductible Health Plans (HDHPs). HSA contribution and plan limits will increase to $4,400 for individual coverage and $8,750 for family coverage. Changes to these limits will take effect January 2026.

HSAs are tax-exempt accounts that help people save money for eligible medical expenses. To qualify for an HSA, the policyholder must be enrolled in an HSA-qualified high-deductible health plan, must not be covered by other non-HDHP health insurance or Medicare, and cannot be claimed as a dependent on a tax return.

Navigating cafeteria plans can be tricky for both employers and employees. A common question is whether financial hardship allows midyear election changes to health FSAs. Unfortunately, it doesn’t.

Why Financial Hardship Isn’t a Qualifying Event

IRS rules state that cafeteria plan elections are irrevocable for the plan year unless a qualifying event occurs. Financial hardship, such as buying a new house and facing unexpected expenses, does not qualify as a permitted election change event.

Qualifying Events for Election Changes

The IRS outlines specific events that allow for midyear election changes, including:

Change in marital status

Change in the number of dependents

Change in employment status

Significant cost or coverage changes (not applicable to health FSAs)

Qualified medical child support orders

Since financial hardship does not fall under these categories, employees must wait until the next open enrollment period to make changes to their health FSA elections.

Communicating Plan Rules

To minimize confusion and potential employee relations issues, employers should clearly communicate the rules and limitations of their cafeteria plans. Providing real-life examples can help employees understand which events qualify for election changes and which do not. This proactive approach can prevent misunderstandings and ensure employees are well-informed.

Plan Design Considerations

Employers may also consider redesigning their health FSA plans to eliminate midyear election changes altogether, except in cases of qualified medical child support orders. This can simplify plan administration and reduce the challenges associated with determining coverage amounts for the remainder of the plan year.

While financial hardship is a difficult situation for any employee, it does not justify a midyear election change to a health FSA under current IRS rules. Employers can support their employees by providing clear communication about plan rules and considering plan design adjustments to streamline administration. By taking these steps, employers can help ensure a smooth and compliant operation of their cafeteria plans.

If your company sponsors a self-insured health plan, you might be wondering whether you still need to pay Patient-Centered Outcomes Research Institute (PCORI) fees. These fees, which fund research on patient-centered outcomes, have been a requirement for several years. However, there have been changes to the legislation that you should be aware of. In this post, we’ll clarify the current requirements for PCORI fees and what you need to do to stay compliant.

What Are PCORI Fees?

PCORI fees are paid by health insurers and sponsors of self-insured health plans. The funds collected are used to support research that helps patients, clinicians, purchasers, and policymakers make informed health decisions.

Legislative Background

Initially, PCORI fees were required for plan and policy years ending before October 1, 2019. For calendar-year plans, this meant that the 2018 plan year was supposed to be the last year for which these fees applied. However, budget legislation passed in 2019 reinstated the PCORI provision, extending the fee requirements through plan years ending before October 1, 2029.

Current Requirements

As of now, if your self-insured health plan’s policy year ends on December 31, 2024, you are required to pay the PCORI fee. This fee is considered an excise tax under the Internal Revenue Code and must be reported on IRS Form 720. Although Form 720 is filed quarterly for other federal excise taxes, the PCORI fee reporting and payment are only required annually. The deadline for filing Form 720 for the 2024 plan year is July 31, 2025.

Record-Keeping

The instructions for Form 720 advise taxpayers to keep their tax returns, records, and supporting documentation for at least four years from the latest of the date the tax became due or the date the tax was paid. This is crucial for ensuring compliance and being prepared for any potential audits.

Conclusion

In summary, PCORI fees are still required for self-insured health plans through plan years ending before October 1, 2029. Make sure to file IRS Form 720 by July 31, 2025, for the 2024 plan year, and keep all related documentation for at least four years. Staying informed and compliant will help your company avoid any penalties and contribute to valuable health outcomes research.

As the FSA grace period draws to a close on March 15, it’s crucial to make the most of your remaining funds. Flexible Spending Accounts (FSAs) offer a fantastic way to save on healthcare expenses, but any unused money will be forfeited if not spent by the deadline. To help you avoid losing your hard-earned dollars, here are five essential items you can purchase with your leftover FSA money:

1. Prescription Eyewear

Why not treat yourself to a stylish new pair of prescription glasses or contact lenses? Not only will you see better, but you’ll also have a chic accessory. Check out the options at the FSA Store.

2. Over-the-Counter Medications

Stock up on everyday essentials like pain relievers, allergy meds, and cold remedies. These are FSA-eligible and super handy to have around. You can find a wide selection at the FSA Store.

3. First Aid Supplies

Be prepared for minor injuries and emergencies by updating your first aid kit. Grab some bandages, antiseptic wipes, and gauze. Check out the FSA Store for all your first aid needs.

4. Health and Wellness Products

Consider investing in health and wellness products like heating pads, hot/cold packs, or even a new humidifier. These items are FSA-eligible and can help you stay comfortable and healthy. Explore the options at the FSA Store.

5. Sunscreen and Skincare Products

Protect your skin by investing in high-quality sunscreen and skincare products. Many of these items are FSA-eligible, making them a smart choice for using up your remaining funds. Check out the FSA Store for some great options.

Don’t let your FSA money go to waste! By purchasing these essential items, you can maximize your savings and ensure you’re well-prepared for the year ahead. Remember to check with your FSA provider for a complete list of eligible expenses and make your purchases before the grace period ends. For a full list of eligible FSA items click here.