When managing a health Flexible Spending Account (FSA) under a cafeteria plan, employers often face questions about reimbursement eligibility—especially when employees incur medical expenses before officially enrolling. A common scenario involves new hires who want to submit claims for services received prior to their start date. So, can a health FSA reimburse expenses incurred before a participant’s enrollment?

Short Answer: No.

According to IRS regulations, a participant must be actively enrolled in the health FSA at the time the medical service is provided for the expense to qualify for reimbursement. This rule applies regardless of when the participant is billed or pays for the service.

Key IRS Guidelines on Health FSA Reimbursements

Coverage Timing Matters: Expenses must be incurred while the employee is covered under the health FSA. Coverage begins on the enrollment date—not retroactively.

Date of Service Is Key: The IRS defines the “incurred date” as the date the medical care is provided, not when payment is made or billed.

No Retroactive Claims: Services received before enrollment (even within the same plan year) are not eligible for reimbursement.

Example Scenario

Let’s say your company has a calendar-year cafeteria plan. An employee is hired in June and enrolls in the health FSA at that time. They later request reimbursement for dental services received in March. Since the services occurred before their enrollment, those expenses cannot be reimbursed under IRS rules.

What About DCAPs (Dependent Care Assistance Programs)?

The same rules apply. DCAPs also require that dependent care services be provided while the participant is enrolled in the plan. Claims for services before enrollment are not eligible.

Best Practices for Employers

Educate Employees Early: Include FSA eligibility and reimbursement rules in onboarding materials.

Review Plan Documents: Ensure your plan clearly outlines coverage start dates and reimbursement criteria.

Encourage Timely Enrollment: Prompt enrollment helps employees maximize their benefits and avoid ineligible claims.

Health FSAs and DCAPs are valuable benefits, but they come with strict IRS rules. Employers must ensure that only expenses incurred during active coverage are reimbursed. Clear communication and proper documentation can help avoid confusion and ensure compliance.

When a former employee receiving COBRA coverage is called to active military duty, employers may wonder how COBRA and USERRA apply. Here’s a quick breakdown of your obligations.

What is COBRA?

COBRA (Consolidated Omnibus Budget Reconciliation Act) allows employees and their families to continue group health coverage for a limited time after job loss or other qualifying events.

What is USERRA?

USERRA (Uniformed Services Employment and Reemployment Rights Act) protects the job and benefit rights of employees who leave work for military service. It includes health coverage continuation—but only for active employees, not those already separated and on COBRA.

Does USERRA Apply in This Case?

No. If the individual is no longer employed and is receiving COBRA, USERRA does not provide additional rights.

Can COBRA Be Terminated Due to TRICARE?

This is a gray area:

IRS rules suggest COBRA may end if the person gains other group coverage (like TRICARE).

DOL guidance says COBRA should not be terminated just because TRICARE is in place.

What Should Employers Do?

Don’t automatically terminate COBRA due to TRICARE.

Check with your insurer or stop-loss carrier to avoid coverage gaps.

Document your decisions and stay updated on federal guidance.

USERRA doesn’t apply to former employees, but COBRA coverage should generally continue—even if TRICARE is now active. When unsure, consult legal or benefits experts to stay compliant.

When employees or their dependents lose group health coverage due to a qualifying event, COBRA ensures they can continue their health benefits. But what happens when a qualified beneficiary under COBRA relocates outside the service area of their HMO (Health Maintenance Organization) plan?

This scenario is more common than you might think—and it’s essential for employers and HR professionals to understand their obligations under COBRA in such cases.

COBRA Basics: Same Coverage Rule

Generally, COBRA requires employers to offer the same health coverage the qualified beneficiary had before the qualifying event. However, there’s a key exception for region-specific plans like HMOs.

The HMO Relocation Exception

If a qualified beneficiary moves out of their HMO’s service area, the employer must offer alternative coverage—but only if certain conditions are met.

✅ When Must Alternative Coverage Be Offered?

Upon Request: The employer must offer other coverage options within a reasonable time after the qualified beneficiary requests it.

Timing: The new coverage must begin no later than the date of relocation or the first day of the following month after the request.

✅ What Coverage Must Be Offered?

If the employer offers other plans (e.g., PPO or indemnity plans) to similarly situated active employees that can be extended to the new location without extraordinary cost, those plans must be offered.

If no such plan exists for similarly situated employees, the employer must offer any available plan that can be extended to the new location.

❌ What If No Coverage Is Available in the New Area?

If no plan can be extended to the new location without extraordinary cost, the employer is not required to offer alternative coverage.

However, if another controlled group member (e.g., a parent or subsidiary company) offers coverage in that area, it may be obligated to provide COBRA coverage.

Extraordinary Costs Are Not Required

Employers are not required to:

Establish new provider networks.

Create new reimbursement schedules.

Offer preferred provider rates in areas without existing employee presence.

If a COBRA participant moves out of their HMO’s service area, you must be prepared to offer alternative coverage options—but only if they are already available to active employees and can be extended without significant cost.

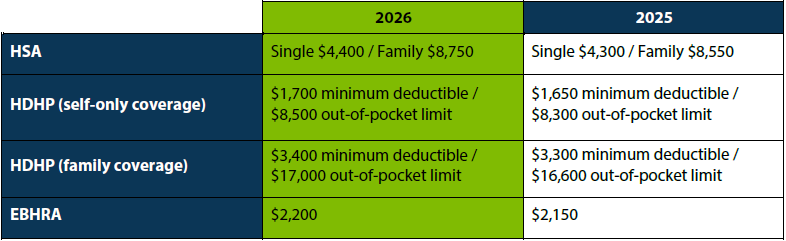

The IRS recently announced the 2026 limits for Health Savings Accounts (HSAs) and High Deductible Health Plans (HDHPs). HSA contribution and plan limits will increase to $4,400 for individual coverage and $8,750 for family coverage. Changes to these limits will take effect January 2026.

HSAs are tax-exempt accounts that help people save money for eligible medical expenses. To qualify for an HSA, the policyholder must be enrolled in an HSA-qualified high-deductible health plan, must not be covered by other non-HDHP health insurance or Medicare, and cannot be claimed as a dependent on a tax return.

Navigating the complexities of the Family and Medical Leave Act (FMLA) can be challenging, especially when it comes to maintaining health coverage for employees on unpaid leave. This guide will help you understand what to do when an employee on FMLA leave fails to pay their health insurance premiums on time, and how it affects Flexible Spending Accounts (FSAs), Health Reimbursement Arrangements (HRAs), Health Savings Accounts (HSAs), and COBRA.

Employer Obligations

Under FMLA, employers must maintain health coverage for employees on leave as if they were still working. This obligation ends if the premium payment is over 30 days late, unless your company policy allows a longer grace period.

Steps Before Dropping Coverage

Before dropping an employee’s health coverage, provide written notice at least 15 days before coverage ends, specifying the termination date if payment isn’t received. Send the notice at least 15 days before the end of the grace period.

Termination of Coverage

Coverage can be terminated retroactively if your company policy allows, otherwise, it ends prospectively at the grace period’s end.

Impact on FSAs, HRAs, and HSAs

FSAs: Employees can choose to continue or revoke their FSA coverage during unpaid FMLA leave. Payment options include pre-pay, pay-as-you-go, and catch-up contributions.

HRAs: Employers must extend COBRA rights to HRAs. Employees can use their HRA balance during COBRA coverage, and employers should calculate a reasonable premium for the HRA.

HSAs: Employees can continue contributing to their HSA during COBRA coverage and use HSA funds to pay for COBRA premiums.

COBRA and ACA Rules

A COBRA election notice isn’t required for coverage loss due to nonpayment. However, failure to return to work after FMLA leave is a COBRA qualifying event. ACA allows cancellation for nonpayment, but stricter state laws may apply.

Restoring Coverage

If an employee returns from FMLA leave after coverage was dropped, their health coverage must be restored.

Managing health coverage for employees on FMLA leave requires careful attention to legal requirements and company policies. By following these steps, you can ensure compliance and support your employees during their leave.