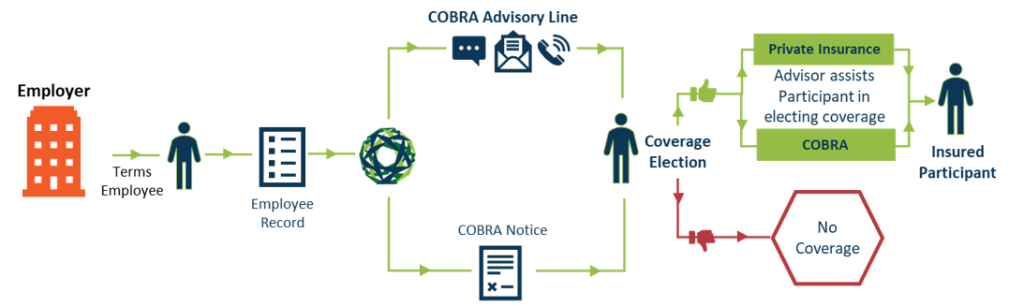

Our new enhanced Cobra solution. COBRAcare+ is a complimentary, cost-saving service offered exclusively by NueSynergy. Participants will get improved engagement through our COBRAcare+ advisory line where they will be guided by a licensed agent to compare COBRA benefits vs. alternative indiviudal health coverage options including subsidies.

QUESTION: We are considering offering a telehealth benefit to our employees that would be separate from our major medical plan. Will this arrangement be an ERISA plan?

ANSWER: Telehealth benefits (also referred to as telemedicine benefits) are often offered under an employer’s group health plan, which is governed by ERISA if sponsored by a private sector employer. Even if telehealth benefits are offered separately from the employer’s group health plan, the benefits are likely subject to ERISA.

In general, an arrangement is an ERISA welfare benefit plan if it is a plan, fund, or program established or maintained by an employer to provide its employees with ERISA-listed benefits. Here is a summary of each element of the definition:

Plan, fund, or program. An arrangement that provides “one-off” benefits and thus does not require an “ongoing administrative scheme” might not be considered a plan, fund, or program subject to ERISA. It is difficult to imagine a telehealth benefit that would not involve ongoing administration, so this element will likely be met.

Established or maintained by an employer for its employees. You have indicated that this benefit would be offered by the company, so this element will be met.

Providing ERISA-listed benefits. Medical benefits are among the benefits listed in ERISA, and telehealth is clearly medical care, so this element will be met.

Under a DOL regulatory safe harbor, certain group insurance arrangements with minimal employer involvement may be exempt from ERISA even if they provide ERISA-listed benefits. If your arrangement is a voluntary employee-pay-all telehealth benefit offered by a third party, with employer involvement limited as set forth in the safe harbor, it would not be an ERISA plan. If it does not meet all the requirements of the safe harbor, it will be an ERISA plan and must comply with the generally applicable rules, such as having a plan administrator, claim and appeal procedures, and a summary plan description.

As a group health plan, a telehealth plan raises legal issues aside from ERISA’s applicability, including considerations under COBRA, HIPAA, and coverage mandates such as first-dollar coverage of preventive services, not imposing annual or lifetime dollar limits on essential health benefits, and parity in mental health and substance use disorder benefits. Note that telehealth-only plans meeting specified criteria have been temporarily exempt from certain of these mandates for certain plan years beginning before the end of the COVID-19 emergency.

Moreover, telehealth coverage may affect an individual’s ability to contribute to a health savings account (HSA), although temporary relief provides that telehealth and other remote care services provided on or after January 1, 2020, will not cause a loss of HSA eligibility for plan years beginning on or before December 31, 2021; for months beginning after March 31, 2022, and before January 1, 2023; and for plan years beginning after December 31, 2022, and before January 1, 2025

Question: During the COVID-19 pandemic, we established a telehealth-only plan to provide benefits to individuals who were not eligible for coverage under our regular group health plan. Can we continue to offer this benefit?

ANSWER: During the COVID-19 pandemic, telehealth-only benefits have been exempt from certain requirements that otherwise apply to group health plans. This relief is linked to the COVID-19 public health emergency (PHE), which appears slated to end on May 11, 2023. Once the exemption is no longer available, a telehealth-only plan may continue but it would have to meet those requirements.

As group health plans, telehealth plans must comply with the many rules applicable to group health plans under ERISA, COBRA, HIPAA, and the Affordable Care Act (ACA). The COVID-19 telehealth relief exempts certain plans from the ACA’s prohibition on annual and lifetime limits and its preventive services mandate—but not from other ACA mandates. The relief applies to any arrangement sponsored by a large employer (generally, one with at least 51 employees) that provides solely telehealth and other remote-care benefits and is offered only to employees or dependents who are not eligible for coverage under any other group health plan offered by that employer.

The relief took effect in 2020 and applies for the duration of any plan year beginning before the end of the COVID-19 PHE. If the PHE ends on May 11, 2023, a calendar year telehealth-only plan could remain covered by the exemption until the end of 2023. But if the plan year is, for example, June 1–May 31, the relief applies only until the end of the current plan year on May 31, 2023; as of June 1, 2023, that plan would have to comply with the preventive services mandate and the prohibition on annual and lifetime limits.

QUESTION: Next year, we plan to amend our company’s cafeteria plan to add a health FSA under which participants elect a coverage amount for the year and pay for it with pre-tax salary reductions. There will be no employer contributions, so participants’ health FSA salary reductions will equal the elected annual coverage amount. The health FSA will be offered to all employees who are eligible for coverage under our major medical, dental, and vision plans. We know that these other plans must offer continuation coverage under COBRA, but will our health FSA also be subject to COBRA?

ANSWER: Unless maintained by a church, the federal government, or a small employer (all employers maintaining the plan must have employed fewer than 20 employees on a typical business day during the preceding calendar year), health FSAs must offer COBRA coverage to all qualified beneficiaries who lose coverage due to a qualifying event and must provide all required COBRA notices. But health FSAs that meet the following three conditions are permitted to provide COBRA coverage on a more limited basis than other group health plans:

Maximum Benefit Condition. The maximum benefit payable under the health FSA during a year to any participant cannot exceed two times the participant’s salary reduction election under the health FSA for the year or, if greater, the salary reduction election plus $500. Your health FSA will satisfy this condition because the annual coverage amount equals the annual salary reduction election.

Availability Condition. Other group health coverage must be available to health FSA participants for the year due to their employment. The other group health coverage must be “major medical” or other coverage that is not limited to excepted benefits (e.g., limited-scope dental or vision coverage). Since all employees eligible for the health FSA will also be eligible for your company’s major medical plan (and assuming that the entry dates for both plans are the same), this condition will be satisfied by plan design.

COBRA Premium Condition. The maximum premium that may be charged for a year of COBRA coverage under the health FSA must equal or exceed the maximum benefit available under the health FSA for the year. Health FSAs funded entirely with participant contributions generally meet this condition because COBRA premiums must be calculated based on the cost to the plan of providing coverage, and the cost to the plan will generally equal the elected annual coverage amount because employees tend to incur claims nearly equal to their elected coverage amounts.

Most, if not all, health FSAs will qualify for the special limited COBRA obligation, and those that do may limit COBRA coverage in two ways: (1) the maximum COBRA coverage period may terminate at the end of the year in which the qualifying event occurs; and (2) the health FSA is not required to offer COBRA coverage to qualified beneficiaries whose accounts are “overspent” as of the date of the qualifying event. An individual’s account is overspent if the remaining annual limit (the difference between the annual election amount and the reimbursable claims submitted before the date of the qualifying event) is less than or equal to the COBRA premiums that would be required for the remainder of the year.