Adoption is a life‑changing journey, but it also comes with significant financial challenges. While the federal adoption tax credit offers meaningful relief, many employees still struggle to cover upfront expenses or fully benefit from the credit. For employers—especially small companies working with tight benefits budgets—the question often becomes: Should we offer adoption assistance benefits when a tax credit already exists?

The short answer: yes. And here’s why.

1. Adoption Expenses Often Exceed the Federal Tax Credit

For 2026, the federal adoption tax credit allows up to $17,670 per child, with up to $5,120 refundable. While helpful, adoption costs can easily surpass these limits. Private domestic, agency, and international adoptions often range from $20,000 to over $50,000.

Employer adoption assistance can help fill this financial gap, reducing out‑of‑pocket expenses for employees and making adoption more accessible.

2. Employees Typically Use the Tax Credit First—But It Doesn’t Replace Employer Support

Because employer‑provided adoption benefits are treated as taxable wages for FICA purposes, most employees will understandably use the tax credit first. The credit usually offers greater financial value upfront.

However, the credit alone rarely covers all expenses—and employees can use both the tax credit and employer reimbursement, as long as it’s not for the same dollar of expense.

Employer benefits remain a critical supplement.

3. Lower‑Income Employees Often Can’t Use the Full Tax Credit

Even with a partially refundable credit, lower-income employees may not have enough tax liability to use the credit’s full value. While unused credits can be carried forward for up to five years, not everyone benefits fully before credits expire.

Employer-provided assistance can help bridge the gap, giving employees meaningful financial support regardless of their tax liability.

Unlike the tax credit—which can only be claimed after finalizing expenses—adoption assistance benefits can provide immediate financial relief. Whether through direct payments or quick reimbursements, employer support can help employees:

Avoid costly personal loans

Manage sudden or large adoption expenses

Reduce financial stress during an emotionally intense process

For many families, improving cash flow is just as valuable as reducing the total cost of adoption.

5. Employers Can Offer Adoption Benefits With Minimal Cost

One major misconception is that offering adoption benefits requires a large employer contribution. In reality, a qualified adoption assistance program can be established with little or no employer funding.

Here’s how:

Employees can use pre‑tax salary reductions to fund adoption expenses through a cafeteria plan.

Special‑needs adoptions receive unique tax treatment—employees may qualify for a full income tax exclusion simply because an employer has a qualifying program in place, even if the employer contributes nothing.

This means even small companies can provide meaningful value at minimal cost.

6. Adoption Benefits Strengthen Recruitment, Retention, and Culture

Appeal to employees who value equity between biological and adoptive parents

Since most employers already subsidize the cost of childbirth through health insurance, offering adoption benefits promotes fairness and signals a genuine commitment to employee well-being.

Even with a federal tax credit in place, employer-provided adoption assistance benefits offer unique financial, emotional, and practical support that the tax credit alone cannot. For many companies—large and small—these benefits are a powerful way to demonstrate values, strengthen your employer brand, and support employees as they grow their families.

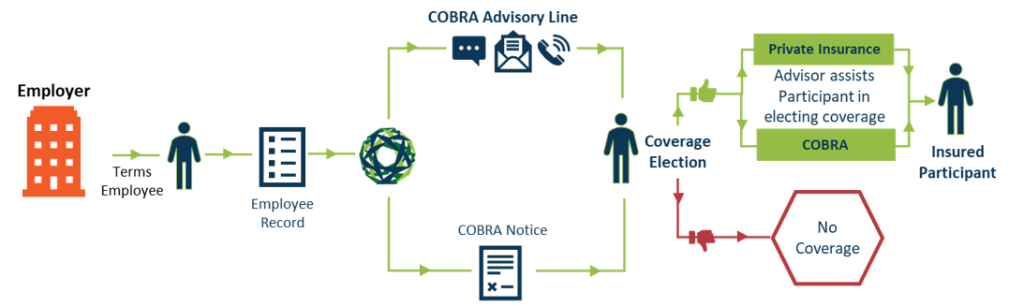

Our new enhanced Cobra solution. COBRAcare+ is a complimentary, cost-saving service offered exclusively by NueSynergy. Participants will get improved engagement through our COBRAcare+ advisory line where they will be guided by a licensed agent to compare COBRA benefits vs. alternative indiviudal health coverage options including subsidies.

QUESTION: We are considering offering a telehealth benefit to our employees that would be separate from our major medical plan. Will this arrangement be an ERISA plan?

ANSWER: Telehealth benefits (also referred to as telemedicine benefits) are often offered under an employer’s group health plan, which is governed by ERISA if sponsored by a private sector employer. Even if telehealth benefits are offered separately from the employer’s group health plan, the benefits are likely subject to ERISA.

In general, an arrangement is an ERISA welfare benefit plan if it is a plan, fund, or program established or maintained by an employer to provide its employees with ERISA-listed benefits. Here is a summary of each element of the definition:

Plan, fund, or program. An arrangement that provides “one-off” benefits and thus does not require an “ongoing administrative scheme” might not be considered a plan, fund, or program subject to ERISA. It is difficult to imagine a telehealth benefit that would not involve ongoing administration, so this element will likely be met.

Established or maintained by an employer for its employees. You have indicated that this benefit would be offered by the company, so this element will be met.

Providing ERISA-listed benefits. Medical benefits are among the benefits listed in ERISA, and telehealth is clearly medical care, so this element will be met.

Under a DOL regulatory safe harbor, certain group insurance arrangements with minimal employer involvement may be exempt from ERISA even if they provide ERISA-listed benefits. If your arrangement is a voluntary employee-pay-all telehealth benefit offered by a third party, with employer involvement limited as set forth in the safe harbor, it would not be an ERISA plan. If it does not meet all the requirements of the safe harbor, it will be an ERISA plan and must comply with the generally applicable rules, such as having a plan administrator, claim and appeal procedures, and a summary plan description.

As a group health plan, a telehealth plan raises legal issues aside from ERISA’s applicability, including considerations under COBRA, HIPAA, and coverage mandates such as first-dollar coverage of preventive services, not imposing annual or lifetime dollar limits on essential health benefits, and parity in mental health and substance use disorder benefits. Note that telehealth-only plans meeting specified criteria have been temporarily exempt from certain of these mandates for certain plan years beginning before the end of the COVID-19 emergency.

Moreover, telehealth coverage may affect an individual’s ability to contribute to a health savings account (HSA), although temporary relief provides that telehealth and other remote care services provided on or after January 1, 2020, will not cause a loss of HSA eligibility for plan years beginning on or before December 31, 2021; for months beginning after March 31, 2022, and before January 1, 2023; and for plan years beginning after December 31, 2022, and before January 1, 2025

QUESTION: One of our employees just noticed that her 2023 pay reflects a salary reduction for DCAP benefits. Initially, she said she never elected DCAP benefits. But when we showed her the DCAP election on her election form, she responded that she had made a mistake in completing the form and asked if we could fix it. Can we do this under the IRS rules?

ANSWER: Possibly, if you conclude that (1) there is “clear and convincing evidence” that your employee made a mistake; (2) the mistake is of a type that can be corrected; and (3) the correction is appropriate. (You may need more information before you can reach these conclusions.) While IRS cafeteria plan regulations do not address election changes for mistakes, IRS officials have informally commented that an employee’s election may be undone when there is clear and convincing evidence of a mistake. Some plans use an “impossibility” approach for evaluating whether such evidence exists, while others use a “facts and circumstances” approach. When the impossibility approach is used, an election change is allowed only if the evidence indicates that it was impossible for the employee to benefit from the mistaken election. For example, you could undo your employee’s DCAP election if she has no qualifying individuals. This approach is more cautious and is easier to administer because it does not involve examining an employee’s intentions or motives.

With the facts-and-circumstances approach, mistakes may be corrected if the plan administrator can reasonably ascertain that a mistake actually occurred. (This may involve inquiry into an employee’s intentions.) When this approach is used, we suggest adopting and consistently following written guidelines that require consideration of factors such as the employee’s past elections and benefit usage (e.g., whether your employee has elected DCAP benefits in the past or has consistently used her spouse’s DCAP); plausible evidence of a clerical mistake (e.g., an employee might easily write $5,000 instead of $500, but it is less likely that $5,000 was written instead of $2,400); assessment of the employee’s truthfulness; proximity to the first payroll date after the new election is in force; and any change in the employee’s circumstances that might indicate reconsideration rather than mistake. In addition, we suggest obtaining a signed certification from the employee describing the mistake and the intended election (e.g., if she intended to elect health FSA benefits instead, the appropriate correction would be an election of such benefits). A plan might also establish a time limit for requests to correct mistaken elections.

Under either approach, if the clear and convincing standard is met, an employee’s clerical, arithmetic, and data-entry errors may be corrected retroactively. (Note that the correction may also involve correcting mistaken payroll withholding.) But mistakes as to a benefit’s scope or tax treatment generally cannot be corrected. For example, your employee could not change her election because she mistakenly believed that the DCAP provided greater tax savings than the dependent care tax credit.

To reduce the likelihood of election mistakes surfacing after the plan year has begun, many employers provide employees with written confirmation of their elections after open enrollment and before the beginning of the new plan year. Employees are instructed to review their elections and notify the employer before the plan year begins if any corrections are needed.