When an employee passes away, employers often face challenging questions regarding benefits and compensation. A common question that arises is whether an employer can pay a deceased employee’s unused Health Reimbursement Arrangement (HRA) balance to the surviving spouse. This article delves into the regulations and best practices surrounding HRAs in such scenarios, ensuring compliance and clarity.

HRAs and Their Restrictions

Health Reimbursement Arrangements (HRAs) are designed to reimburse employees for qualifying medical expenses, as outlined in Code § 213(d). Importantly, HRAs are not allowed to disburse cash payments to employees or their beneficiaries at any time, including after the employee’s death. Any attempt to convert HRA balances into cash would disqualify the HRA for all participants, rendering all reimbursed amounts taxable—even those for legitimate medical expenses.

The Concept of Post-Death Spend-Downs

While direct cash payments are prohibited, HRAs can include a provision known as a post-death “spend-down.” This feature allows the remaining HRA balance to be used to cover qualifying medical expenses for the deceased employee’s surviving spouse, tax dependents, and qualifying children. Employers should check their HRA plan documents to see if this feature is included and, if not, consider amending the plan to incorporate it.

Compliance and Nondiscrimination Rules

Amending an HRA plan to include a post-death spend-down feature must comply with several nondiscrimination rules. These rules ensure that benefits are not skewed in favor of highly compensated individuals. Specifically, all benefits provided to highly compensated participants must also be made available to all other participants.

Additionally, IRS Notice 2015-87 casts some uncertainty on whether family members without major medical coverage can utilize a post-death spend-down feature. Until further clarification from the IRS, a cautious approach would be to limit these reimbursements to family members who also have major medical coverage.

Administering Post-Death Spend-Downs

Proper administration of the post-death spend-down feature is crucial. Only qualifying medical expenses for eligible individuals should be reimbursed. Failure to adhere to this can result in all HRA reimbursements becoming taxable, not just those for ineligible expenses. Employers must also remember their obligations under COBRA. If a deceased employee’s death triggers a COBRA qualifying event, then qualified beneficiaries must be given the opportunity to continue their HRA coverage for the duration prescribed by COBRA, regardless of the presence of a post-death spend-down feature.

Conclusion

While it may seem compassionate to pay out a deceased employee’s unused HRA balance to their surviving spouse, doing so would jeopardize the tax-advantaged status of the HRA for all participants. Instead, employers should explore the option of a post-death spend-down feature, ensuring they comply with all relevant nondiscrimination rules and administrative guidelines. By carefully navigating these regulations, employers can support their employees’ families while maintaining the integrity of their HRA plans.

The Consolidated Omnibus Budget Reconciliation Act (COBRA) provides employees with the option to continue health insurance coverage after leaving their job. However, certain circumstances, such as gross misconduct, can affect the availability of this coverage. This blog post explores a unique case where an employee’s gross misconduct was discovered after retirement and the implications for COBRA coverage.

The Case

Three months ago, a bookkeeper retired from a company, electing COBRA coverage under the company’s medical plan. Recently, it was discovered that she had embezzled thousands of dollars during her tenure. The question arose: Could the company retroactively terminate her COBRA coverage due to this gross misconduct?

The Verdict

The short answer is probably not. While COBRA coverage need not be offered to employees terminated due to gross misconduct, in this case, the bookkeeper voluntarily retired and elected COBRA before her misconduct was discovered.

The Legal Perspective

If an employee is terminated for gross misconduct, there is no COBRA qualifying event for the employee or any covered dependents. However, employers should exercise caution when denying COBRA coverage due to gross misconduct. This is because COBRA does not clearly define “gross misconduct,” and courts have not agreed on a common standard. Therefore, denying COBRA coverage due to gross misconduct carries a higher-than-usual risk of litigation.

The After-Acquired Evidence

In this case, the company faces an additional obstacle. While embezzlement likely constitutes gross misconduct for COBRA purposes, the employee’s termination was due to voluntary retirement, not gross misconduct. Courts generally evaluate an employer’s decision to deny COBRA based on evidence available at the time of the employee’s discharge. The use of after-acquired evidence of gross misconduct to justify termination of employment has been rejected by the U.S. Supreme Court and several other courts in the COBRA context. Therefore, it is unlikely that a court would allow COBRA coverage to be terminated—retroactively or going forward—when gross misconduct is discovered after an employee has elected COBRA.

Conclusion

This case serves as a reminder for employers to consult with legal counsel and insurers when considering the denial of COBRA coverage due to gross misconduct. It also highlights the complexities involved in COBRA coverage termination, especially when evidence of misconduct is discovered post-employment. As always, each case is unique and should be evaluated on its own merits.

Providing a Summary of Benefits and Coverage (SBC) that is culturally and linguistically appropriate is not just a good practice—it’s a legal requirement for many group health plans. Whether your plan is self-insured or fully insured, it’s essential to understand and comply with these regulations to avoid penalties and ensure your members can access and understand their benefits. In this blog post, we’ll break down what you need to know about furnishing the SBC in languages other than English.

Understanding the Requirement

The SBC must be presented in a “culturally and linguistically appropriate” manner. This requirement is part of a broader effort to ensure that individuals who are literate only in a non-English language can understand their health coverage options. The specific conditions under which this requirement is triggered are based on U.S. Census data.

When Does the Requirement Apply?

The requirement applies if your plan’s SBC is provided to individuals in any county where at least 10% of the population is literate only in the same non-English language. The Department of Health and Human Services (HHS) regularly updates a list of such counties and the languages that apply. As of January 1, 2025, a new list will come into effect, and it’s crucial for plan administrators to stay updated with these changes.

Compliance Steps for Group Health Plans

To comply with the “culturally and linguistically appropriate” requirement, follow these steps:

Identify Applicable Counties: Check the latest HHS list to see if any counties where your plan members reside meet the 10% threshold for non-English language literacy.

Provide Interpretive Services: In applicable counties, offer interpretive services in the relevant languages. This includes answering questions and providing assistance in the non-English language.

Include a One-Sentence Statement: On the SBC, include a one-sentence statement in the applicable non-English languages. This statement should clearly indicate how to access language services. It must be placed on the same page as the “Your Rights to Continue Coverage” and “Your Grievance and Appeals Rights” sections.

Offer Written Translations: Upon request, provide a written translation of the SBC in the applicable non-English language. The agencies have provided an SBC template that includes this one-sentence statement in all required languages for plan years beginning before 2025.

Stay Updated: Keep an eye on updates from the HHS, DOL, and IRS regarding additional translations and template updates. These resources will assist in maintaining compliance with the latest requirements.

Voluntary Compliance

Even if your plan does not operate in a county meeting the 10% threshold, you may choose to include the one-sentence statement in any non-English language. If you opt for this, ensure you are prepared to provide the necessary language services.

Differentiating SBC Requirements from ERISA

It’s important to note that the requirements for SBCs differ from ERISA’s rules on language assistance for Summary Plan Descriptions (SPDs) and Summary of Material Modifications (SMMs). Ensure you are familiar with both sets of regulations to avoid confusion and non-compliance.

Meeting the requirement for a culturally and linguistically appropriate SBC is vital for compliance and member satisfaction. By following the steps outlined above, your self-insured group health plan can ensure that all members understand their coverage options, regardless of their primary language. Stay informed, be proactive, and provide the necessary language services to comply with federal regulations and support your diverse member base.

Summer is right around the corner (June 21)! Whether you have plans to travel or are staying closer to home, your Flexible Spending Account can help you stock up on summer essentials without breaking the bank. Depending on your activity, your FSA can provide a variety of products! Below is a list of the top items to not only enhance your summer experience but also ensure your health and wellness.

Sunscreen

Sunscreen is a no-brainer when it comes to summer. With more time spent outdoors, protecting your skin from harmful UV rays is crucial. The last thing you want to worry about before heading to the beach or the pool is sunscreen. Buying sunscreen while on vacation can also be more expensive. Click here for all FSA eligible sunscreen bundle options.

First Aid

Whether you are dealing with mosquito bites, blisters from those long summer walks, or minor cuts and scrapes, accidents happen and being prepared is key. Click here for all FSA eligible medicine and treatment care.

Shoe Inserts

Comfortable footwear is essential for enjoying summer activities. A shoe insert can help reduce foot pain offering extra padding and improve blood circulation. Click here for all FSA eligible foot care options.

Eye Care

Protecting your eyes is just as important as protecting your skin. If you wear contact lenses, you want them to stay comfortable and clean. The FSA store offers a variety ofcontact lens solution and eye drops to make sure your eyes don’t get irritated throughout the days. Let’s not forget about the UV rays! The FSA store also offers sunglasses with or without prescription!

Your FSA is more than just a healthcare benefit; it’s a gateway to a healthier, more enjoyable summer. By investing in these FSA-eligible essentials, you’re not only making smart financial choices but also ensuring that you and your family can fully embrace all the joys that summer has to offer. So, dive into the season with confidence, knowing that you’re covered for every sunny day ahead.

For all FSA eligible items, or other HRA and HSA eligible items, click here.

Note: The products mentioned are based on the latest available information and are subject to change. Always check with your FSA provider for the most current eligibility list.

Understanding cafeteria plan election changes can be complex, especially when dealing with domestic partner relationships. Here’s what you need to know about whether such relationships qualify for election changes under cafeteria plan rules.

Domestic Partner Relationship and Election Changes

The commencement of a domestic partner relationship does not qualify as a “change in marital status” under cafeteria plan rules. Legal marital status changes include marriage, death of a spouse, divorce, legal separation, and annulment. While the list is not exhaustive, the IRS does not recognize the start or end of a domestic partner relationship as equivalent to these events.

Alternative Election Change Event: Change in Coverage Under Another Employer Plan

However, another permitted event, “change in coverage under another employer plan,” may allow for an election change. If your plan includes this provision, your employee can drop major medical coverage upon becoming covered under their partner’s employer plan. This event does not restrict changes to the plans maintained by the employer of a spouse or dependent but does not allow changes to health FSA elections.

Key Takeaways

Domestic Partner Relationship: Does not qualify as a change in marital status for election changes.

Change in Coverage: Employees can change their election if covered under a partner’s employer plan.

Documentation: Required to prove new coverage under the partner’s employer plan.

Plan Specifics: Check your specific cafeteria plan terms for detailed rules and procedures.

Conclusion

While domestic partner relationships don’t qualify for election changes under marital status rules, a change in coverage under another employer plan can allow adjustments. Always consult your cafeteria plan specifics and seek professional advice for compliance.

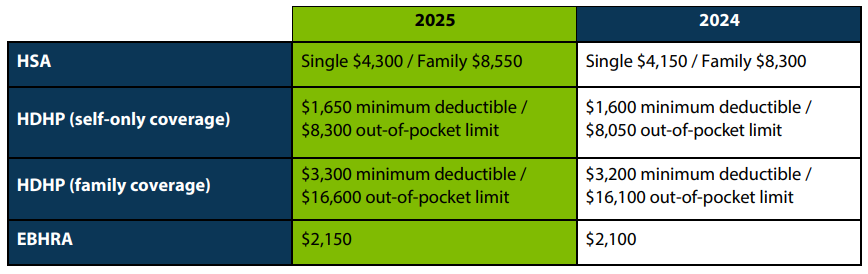

The IRS recently announced the 2025 limits for Health Savings Accounts (HSAs) and High Deductible Health Plans (HDHPs). HSA contribution and plan limits will increase to $4,300 for individual coverage and $8,550 for family coverage. Changes to these limits will take effect January 2025.

HSAs are tax-exempt accounts that help people save money for eligible medical expenses. To qualify for an HSA, the policyholder must be enrolled in an HSA-qualified high-deductible health plan, must not be covered by other non-HDHP health insurance or Medicare, and cannot be claimed as a dependent on a tax return.